Here’s an introduction to an article on «How to Use Peer Lending as a Tool for Debt Consolidation»:

**Option 1 (Focuses on the Problem):**

Are you drowning in debt? High-interest credit card balances, personal loans, and medical bills can feel overwhelming. But there’s a potential solution that doesn’t involve a bank: peer lending. This innovative financing model lets you borrow directly from individuals, often at lower interest rates than traditional lenders. In this article, we’ll explore how peer lending can be a powerful tool for debt consolidation, helping you take control of your finances and achieve financial freedom.

**Option 2 (Focuses on the Solution):**

Tired of paying sky-high interest rates on your debt? Peer lending might be the answer you’ve been looking for. By connecting borrowers directly with individual lenders, peer-to-peer platforms offer a unique way to secure loans with competitive rates and flexible terms. This article will guide you through the process of using peer lending to consolidate your debt, simplify your payments, and potentially save you thousands of dollars in interest.

Aquí tienes un subtítulo H2 y 5 subtítulos H3 con información detallada sobre el uso del préstamo entre pares para la consolidación de deudas, incluyendo tablas para mayor claridad:

Harnessing Peer Lending for Debt Consolidation: A Step-by-Step Guide

What is Peer Lending?

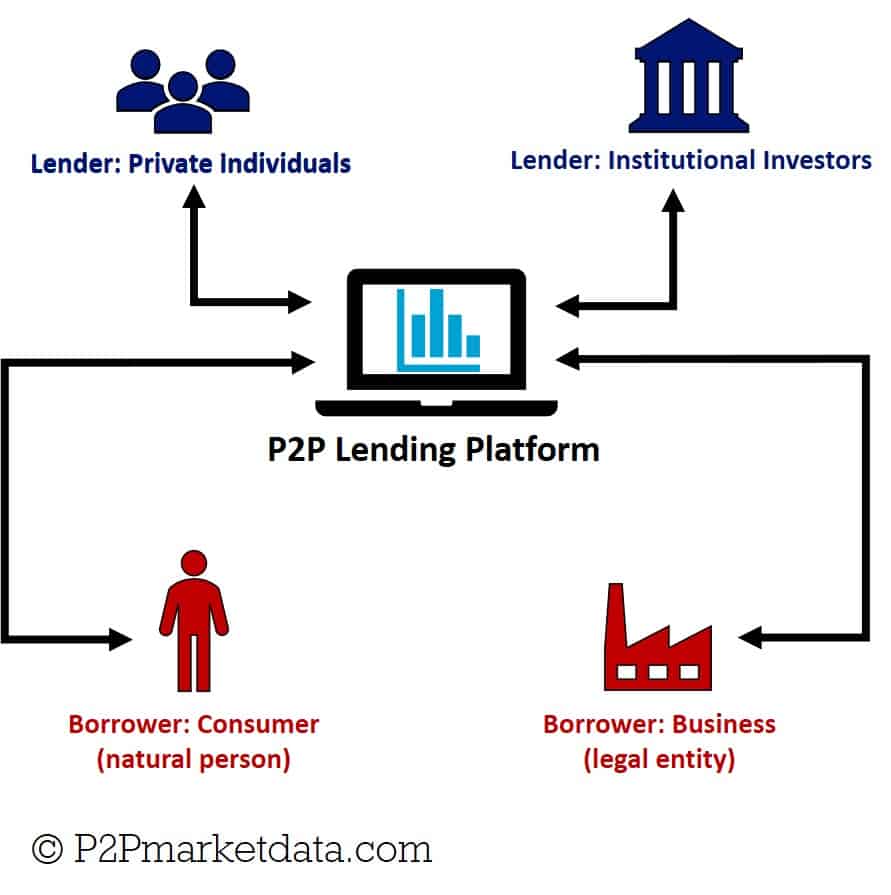

Peer-to-peer (P2P) lending is a form of online lending where individuals or businesses borrow money directly from other individuals or businesses, bypassing traditional financial institutions. P2P platforms act as intermediaries, connecting borrowers with lenders and facilitating the loan process.

How Does Peer Lending Work for Debt Consolidation?

Peer lending can be a valuable tool for debt consolidation by:

Securing a lower interest rate: P2P loans often have lower interest rates than traditional credit cards or personal loans, especially for borrowers with good credit scores.

Simplifying payments: You can consolidate multiple debts into a single monthly payment, making it easier to manage your finances.

Getting a larger loan amount: P2P platforms may offer higher loan amounts compared to traditional institutions, allowing you to cover more debts.

| Traditional Debt Consolidation | Peer-to-Peer Debt Consolidation |

|---|---|

| Typically involves a personal loan from a bank or credit union | Involves taking out a loan from individuals through a P2P platform |

| Interest rates may be higher | Interest rates may be lower, especially for borrowers with good credit |

| May require a longer application process | Application process can be faster and more streamlined |

Key Benefits of Using Peer Lending for Debt Consolidation

Potential for lower interest rates: As mentioned above, P2P loans often have lower interest rates than traditional debt consolidation options. This can save you significant money on interest payments over the life of the loan.

Flexibility: P2P platforms offer a variety of loan terms and conditions, making it easier to find a loan that fits your individual needs.

Transparency: Most P2P platforms are transparent about their fees and interest rates, allowing you to make an informed decision.

Convenience: The entire process, from application to funding, can be done online, saving you time and effort.

Factors to Consider Before Using Peer Lending for Debt Consolidation

Credit score: Your credit score plays a significant role in determining your eligibility for a P2P loan and the interest rate you’ll be offered. A higher credit score typically leads to lower interest rates.

Loan amount: P2P platforms have loan amount limits, so ensure you can get a loan large enough to cover all your existing debts.

Loan terms: Carefully review the loan terms and conditions, including the interest rate, repayment period, and any fees associated with the loan.

Platform reputation: Not all P2P platforms are created equal. Research and choose a platform with a good reputation for transparency, security, and customer service.

How to Choose the Right Peer Lending Platform

Compare interest rates and fees: Look at the interest rates and fees charged by different P2P platforms and choose one that offers the most competitive rates.

Read reviews: Check online reviews from other borrowers to get an idea of the platform’s reputation and customer service.

Consider loan terms: Look for a platform that offers loan terms that align with your financial needs and goals.

Check for security measures: Ensure the platform uses strong security measures to protect your personal and financial information.

Remember, debt consolidation should be a strategic move to improve your financial health. Carefully consider all the factors involved before making a decision.

What is the minimum credit score for peer-to-peer lending?

What is a Peer-to-Peer (P2P) Loan?

A peer-to-peer (P2P) loan is a type of loan that is made directly from one person to another, without the involvement of a traditional financial institution. Instead of going through a bank, you borrow money from an individual or a group of individuals who invest in the loan through a P2P lending platform. These platforms act as intermediaries, connecting borrowers and lenders, and facilitating the loan process.

What is the Minimum Credit Score for Peer-to-Peer Lending?

There is no one-size-fits-all answer to this question, as the minimum credit score required for peer-to-peer lending can vary significantly between different lenders. However, most P2P lenders require a minimum credit score of at least 620 to qualify for a loan. Some platforms may have lower credit score requirements for certain types of loans, such as secured loans or loans with higher interest rates.

Factors Affecting Minimum Credit Score Requirements

- Lender’s Policies: Each P2P lender sets its own minimum credit score requirements. Some lenders may focus on borrowers with higher credit scores, while others may be more open to lending to individuals with lower credit scores.

- Loan Type: The type of loan you are applying for can also influence the minimum credit score requirement. Secured loans, which are backed by collateral, typically have lower credit score requirements than unsecured loans.

- Loan Amount: The amount of money you are borrowing can also affect the minimum credit score required. Larger loan amounts often require higher credit scores.

- Interest Rate: Loans with higher interest rates may have lower credit score requirements, as lenders are willing to take on more risk with these loans.

How to Improve Your Credit Score for Peer-to-Peer Lending

- Pay Your Bills On Time: Late payments are a major factor that can negatively impact your credit score. Make sure to pay all your bills on time, including credit card bills, utility bills, and loan payments.

- Keep Your Credit Utilization Low: Your credit utilization ratio is the amount of credit you are using compared to your available credit. It is recommended to keep your credit utilization ratio below 30%.

- Don’t Open Too Many New Accounts: Each time you apply for a new credit card or loan, it results in a hard inquiry on your credit report. Too many hard inquiries can lower your credit score.

- Monitor Your Credit Report: You should monitor your credit report regularly for any errors. You can obtain free copies of your credit report from all three credit bureaus (Equifax, Experian, and TransUnion) at AnnualCreditReport.com.

Tips for Finding a Peer-to-Peer Lender

- Compare Interest Rates: Different P2P lenders offer varying interest rates. It is crucial to compare interest rates from multiple lenders to secure the best deal.

- Read Reviews: Check online reviews from previous borrowers to gain insights into the reputation and customer service of different P2P lenders.

- Consider Fees: Some P2P lenders charge origination fees, late payment fees, or other fees. Ensure you understand all the fees associated with a loan before you apply.

Which type of loan can be used for debt consolidation?

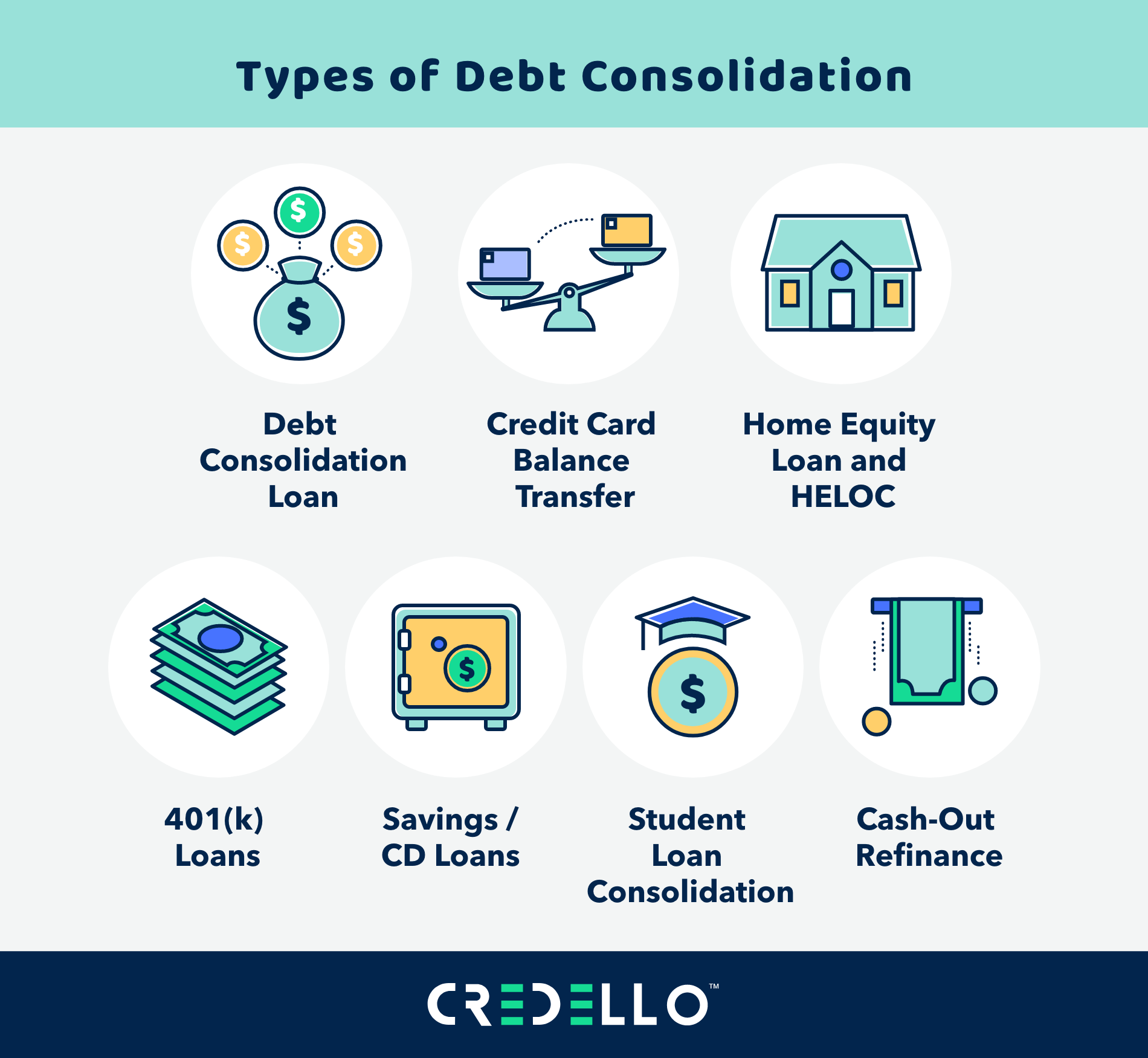

Debt Consolidation Loans

A debt consolidation loan is a type of personal loan that allows you to borrow money to pay off multiple debts, such as credit cards, medical bills, or payday loans. This can help simplify your finances by reducing the number of payments you have to make and potentially lowering your overall interest rate.

Types of Debt Consolidation Loans

There are several types of debt consolidation loans available, including:

- Personal loans: These loans are typically unsecured, meaning they are not backed by collateral. They offer fixed interest rates and terms, making them predictable and manageable.

- Balance transfer credit cards: These cards allow you to transfer balances from other credit cards to the new card, often with a 0% introductory APR for a set period. This can save you money on interest if you can pay off the balance within the introductory period.

- Home equity loans and lines of credit (HELOCs): These loans are secured by your home, meaning they have lower interest rates than unsecured loans. However, you risk losing your home if you default on the loan.

- Debt settlement programs: These programs negotiate with your creditors to reduce the amount of debt you owe. However, they can come with high fees and may negatively impact your credit score.

How Debt Consolidation Works

When you take out a debt consolidation loan, the lender pays off your existing debts with the loan proceeds. You then make a single monthly payment to the lender, covering both the principal and interest on the new loan.

Benefits of Debt Consolidation

There are several potential benefits of debt consolidation:

- Lower interest rates: You may be able to secure a lower interest rate on a debt consolidation loan than you have on your existing debts, which can save you money on interest payments.

- Simplified payments: Instead of making multiple payments to different creditors, you only have to make one payment to the lender.

- Improved credit score: By paying off your debts on time, you can improve your credit score.

Things to Consider Before Consolidating Debt

There are some things to consider before taking out a debt consolidation loan:

- Interest rate: Make sure the interest rate on the consolidation loan is lower than the interest rates on your existing debts.

- Fees: Some lenders charge origination fees or other fees, so be sure to factor those into the cost of the loan.

- Credit score: Your credit score will affect the interest rate and terms you qualify for.

Can individuals use P2P lending?

What is P2P lending?

P2P lending, also known as peer-to-peer lending, is a form of online lending that allows individuals to borrow and lend money directly from each other, bypassing traditional financial institutions like banks. This is facilitated through online platforms that connect borrowers and lenders, enabling them to negotiate loan terms and complete transactions.

Absolutely! P2P lending is specifically designed for individuals to participate as both borrowers and lenders. This means individuals can access loans from other individuals, potentially offering more flexible terms or lower interest rates compared to traditional loans. Conversely, individuals can also invest their money by lending to other individuals, earning interest on their investments.

How can individuals use P2P lending for borrowing?

Individuals can use P2P lending platforms to apply for various loan purposes, such as:

- Debt consolidation: Combining multiple debts into a single loan with potentially lower interest rates.

- Home improvement: Financing home renovations or repairs.

- Medical expenses: Covering unexpected medical costs.

- Personal loans: Funding major purchases or covering unexpected expenses.

- Business loans: Starting or growing a small business.

How can individuals use P2P lending for lending?

Individuals can choose to invest in P2P loans through various options, including:

- Individual loans: Directly choosing specific borrowers and loan terms.

- Automated investments: Using algorithms to distribute investments across a diversified portfolio of loans.

- Fixed-income investments: Investing in loan portfolios with predetermined interest rates and maturities.

What are the benefits of using P2P lending for individuals?

P2P lending offers potential benefits for individuals, such as:

- Lower interest rates for borrowers: Potentially more favorable rates compared to traditional loans.

- Faster approval times: Online platforms often offer quicker loan processing.

- Greater flexibility: Customized loan terms to suit individual needs.

- Higher potential returns for lenders: Potential for higher interest rates compared to traditional savings accounts.

- Diversification of investment portfolio: Opportunity to diversify investments beyond traditional assets.

What are the disadvantages of peer-to-peer lending?

Potential for Higher Interest Rates

Peer-to-peer lending platforms often charge higher interest rates than traditional banks. This is because they have to cover their operating costs and make a profit, and they also have to account for the higher risk involved in lending to borrowers who may not be able to get loans from traditional lenders.

- Higher interest rates can make P2P loans more expensive than traditional loans.

- P2P platforms may charge higher fees for origination and other services.

Risk of Default

There is always a risk that borrowers will default on their P2P loans. This can happen for a variety of reasons, such as job loss, illness, or unexpected expenses. If a borrower defaults, investors may lose some or all of their investment.

- Investors are exposed to the risk of losing their principal investment.

- P2P platforms may not have adequate mechanisms to collect on defaulted loans.

Lack of Regulation

The P2P lending industry is relatively unregulated, which means that there are fewer protections for investors. This can make it more difficult to find reliable and trustworthy platforms.

- There is a lack of regulatory oversight in some jurisdictions.

- P2P platforms may not be subject to the same level of scrutiny as banks and other financial institutions.

Limited Access to Funding

Some P2P platforms may have limited access to funding, which can make it difficult for borrowers to obtain the loans they need.

- P2P platforms may not have as much capital as traditional lenders.

- Investors may be hesitant to invest in P2P loans due to the risks involved.

Lack of Transparency

It can be difficult to assess the creditworthiness of borrowers on P2P platforms, as they may not have access to the same level of information that traditional lenders have. This can make it difficult to determine the risk of investing in P2P loans.

- P2P platforms may not disclose all of the information investors need to make informed decisions.

- It can be difficult to compare different P2P platforms and their loan offerings.

Frequently Asked Questions

What is peer-to-peer lending, and how does it work?

Peer-to-peer lending, also known as social lending, is a form of alternative finance where individuals lend money to other individuals or businesses through an online platform. This disintermediates the traditional financial institutions and allows direct lending between borrowers and lenders. Here’s how it works:

1. Borrowers: Borrowers submit a loan request on a peer-to-peer lending platform. This request includes details about the loan purpose, amount, interest rate, and repayment period.

2. Lenders: Lenders browse available loan requests and choose which ones they want to fund based on their risk appetite and desired return.

3. Loan Matching: The platform matches borrowers and lenders based on their creditworthiness, loan requirements, and investment preferences.

4. Loan Disbursement: Once the loan is matched, the platform disburses the funds to the borrower.

5. Repayment: The borrower makes monthly repayments to the platform, which then distributes the funds to the lenders.

How can I use peer-to-peer lending to consolidate my debt?

Debt consolidation is the process of combining multiple debts into a single loan with a lower interest rate. Peer-to-peer lending can be a useful tool for debt consolidation because it often offers lower interest rates than traditional credit cards or personal loans. Here’s how it works:

1. Borrow a Loan: You can take out a peer-to-peer loan and use the funds to pay off your existing debts.

2. Consolidation: The loan payments will be made to the platform, which then distributes the funds to your creditors, effectively consolidating your debts into one.

3. Lower Interest: If you secure a lower interest rate with a peer-to-peer loan, you will save money on interest charges over time.

4. Streamlined Payments: You’ll only have one monthly payment to make instead of multiple, making debt management easier.

What are the advantages and disadvantages of using peer-to-peer lending for debt consolidation?

Peer-to-peer lending offers several advantages for debt consolidation, but it also comes with some drawbacks:

Advantages:

Lower Interest Rates: Peer-to-peer lending platforms often have lower interest rates than traditional lenders, which can save you money on interest charges over time.

Flexibility: You can often find loans with flexible repayment terms to suit your individual needs.

Faster Approval: Peer-to-peer lending applications are often processed faster than traditional loans.

Disadvantages:

Higher Risk: Peer-to-peer loans can be riskier than traditional loans because they are not insured by the government.

Limited Availability: Not everyone qualifies for peer-to-peer loans, and they may not be available in all states.

Potential for Scams: It is important to choose a reputable platform to avoid scams.

What factors should I consider when choosing a peer-to-peer lending platform?

When choosing a peer-to-peer lending platform for debt consolidation, there are several key factors to consider:

Interest Rates: Compare interest rates from different platforms to find the lowest rates available.

Fees: Check for any origination fees, late payment fees, or other fees associated with the loan.

Credit Requirements: Make sure you meet the platform’s creditworthiness requirements.

Reputation: Research the platform’s reputation and read reviews from other borrowers.

Security: Ensure the platform has strong security measures to protect your personal and financial information.

Customer Service: Look for a platform with excellent customer service and support.

By carefully considering these factors, you can choose a peer-to-peer lending platform that meets your needs and helps you achieve your debt consolidation goals.