Saving money can seem daunting, especially when you feel like you’re barely scraping by. But the truth is, everyone can save, regardless of their income level. The key is to set realistic goals that work for your unique financial situation. This article will guide you through the process of setting achievable savings goals based on your income, expenses, and financial aspirations. We’ll explore strategies for maximizing your savings potential and creating a plan that feels manageable and motivating. Get ready to take control of your finances and build a brighter financial future!

Aquí tienes un subtítulo H2, 5 subtítulos H3 y tablas para un artículo sobre cómo establecer objetivos de ahorro realistas para tu nivel de ingresos:

How to Set Realistic Savings Goals for Your Income Level

1. Determine Your Income and Expenses

Knowing your income and expenses is crucial for setting achievable savings goals. It’s important to understand how much money you bring in each month and where it goes. This information will help you identify areas where you can cut back and free up more money for savings.

| Income | Expense | Description |

|---|---|---|

| Salary | Rent/Mortgage | Cost of housing |

| Part-time income | Utilities | Electricity, water, gas |

| Investment income | Groceries | Food and beverages |

| Transportation | Car payments, gas, public transport | |

| Healthcare | Insurance, medical expenses | |

| Entertainment | Dining out, movies, hobbies |

2. Consider Your Financial Goals

Think about your financial goals, both short-term and long-term. This will help you decide how much you need to save and for what purpose. Some common financial goals include:

| Short-Term Goals | Long-Term Goals |

|---|---|

| Emergency fund | Retirement savings |

| Down payment on a house | College savings |

| Vacation | Investment portfolio |

3. Start Small and Gradually Increase

It’s important to start with a small and achievable savings goal. Don’t try to save too much too quickly, as this can lead to frustration and discouragement. As you get used to saving, you can gradually increase your savings amount.

| Savings Strategy | Description |

|---|---|

| Start with 5% of your income | A manageable starting point for most people |

| Increase savings by 1% every few months | Gradual increase to help you adjust |

4. Automate Your Savings

One of the easiest ways to save money consistently is to automate your savings. This means setting up automatic transfers from your checking account to your savings account on a regular basis.

| Automation Method | Description |

|---|---|

| Direct deposit | A portion of your paycheck goes directly to savings |

| Recurring transfers | Scheduled transfers from your checking to savings account |

5. Track Your Progress and Adjust as Needed

It’s important to track your progress and make adjustments to your savings goals as needed. Review your savings plan regularly and make sure it’s still on track to meet your financial goals. You may need to adjust your savings amount or expenses to stay on target.

| Tracking Methods | Description |

|---|---|

| Budgeting apps | Track income, expenses, and savings automatically |

| Spreadsheets | Manually track your finances and progress |

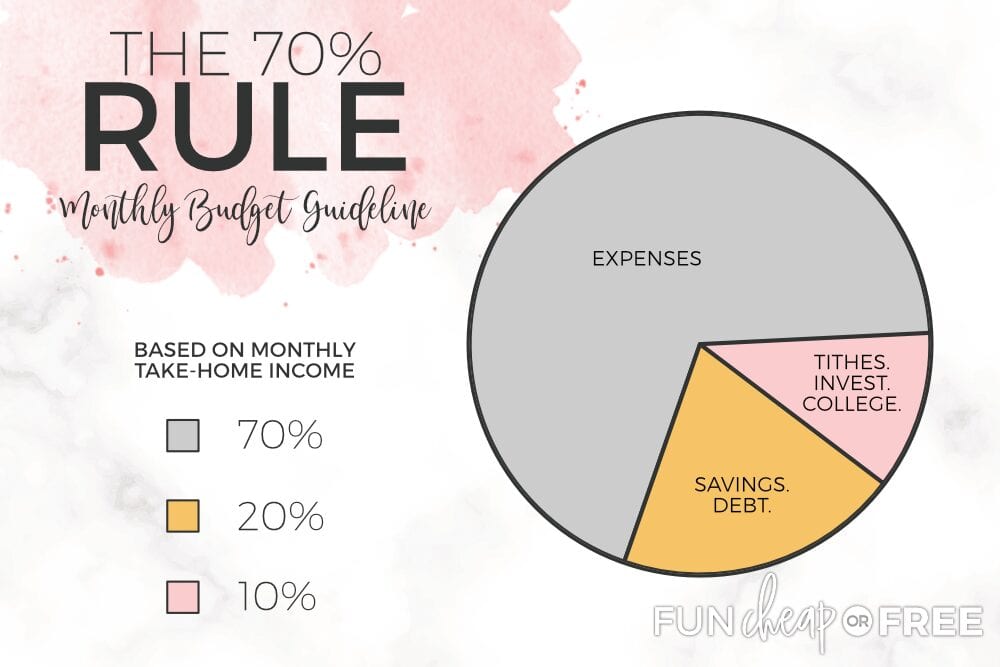

What is the 70 30 20 rule for savings?

The 70 30 20 rule is a budgeting guideline that suggests dividing your after-tax income into three categories: needs, wants, and savings.

Needs: These are the essential expenses required for survival, such as housing, food, utilities, transportation, and healthcare. The rule suggests allocating 70% of your income to cover these needs.

Wants: These are discretionary expenses that are not essential for survival but provide enjoyment or convenience, such as entertainment, dining out, clothing, and travel. You should allocate 30% of your income to cover these wants.

Savings: This category includes both short-term savings for emergencies and long-term savings for retirement or other financial goals. The rule suggests allocating 20% of your income to savings.

Why is the 70 30 20 rule important?

The 70 30 20 rule is important because it encourages financial discipline and prioritizes saving.

It provides a simple framework for budgeting and helps individuals manage their finances more effectively.

By allocating a significant portion of income to savings, it allows people to build a financial safety net and achieve their long-term financial goals.

The rule also helps individuals avoid unnecessary debt and make informed spending decisions.

How to implement the 70 30 20 rule

Implementing the 70 30 20 rule requires tracking your income and expenses carefully.

Track your income and expenses: Use a budgeting app, spreadsheet, or notebook to keep track of your income and spending.

Allocate your income: Divide your after-tax income into three categories: needs, wants, and savings.

Adjust your spending: Review your expenses regularly and adjust your spending habits as needed to stay within your budget.

Automate your savings: Set up automatic transfers from your checking account to your savings account on a regular basis.

Is the 70 30 20 rule right for everyone?

The 70 30 20 rule is a general guideline, and it may not be suitable for everyone.

Your individual needs and circumstances: Factors such as your income level, debt obligations, and financial goals can influence how you allocate your income.

Flexibility: The rule can be adapted to fit your specific needs. For example, you may choose to allocate a higher percentage of your income to savings or a lower percentage to wants.

Professional advice: If you’re unsure how to implement the 70 30 20 rule or have complex financial needs, consider seeking advice from a financial advisor.

Benefits of the 70 30 20 rule

The 70 30 20 rule offers several potential benefits for individuals seeking to improve their financial well-being.

Increased savings: Allocating a substantial portion of income to savings can accelerate the accumulation of wealth.

Reduced debt: By prioritizing needs and wants over unnecessary spending, the rule can help individuals avoid excessive debt.

Improved financial security: A well-funded emergency fund and long-term savings provide a safety net and financial stability.

Greater control over finances: The rule promotes budgeting discipline and empowers individuals to take control of their finances.

Reduced financial stress: By following a structured budgeting framework, individuals can experience reduced financial stress and worry.

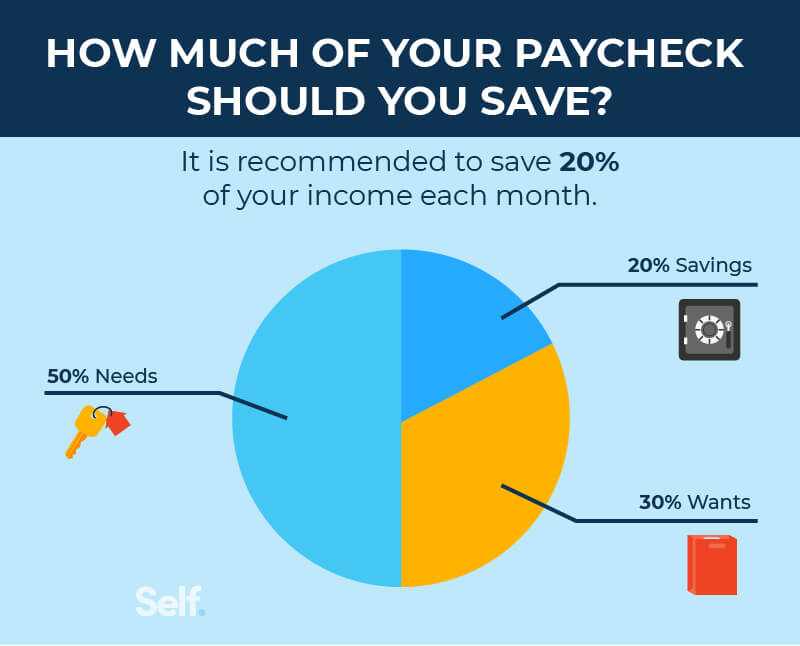

How much of your income can you realistically save?

It is impossible for me to provide a specific answer to this question as I do not have access to your personal financial situation. The amount you can realistically save depends on a variety of factors, including your income, expenses, and financial goals.

Factors to consider when determining your savings rate

- Income: Your income is the starting point for determining how much you can save. The more money you earn, the more you have available to save.

- Expenses: Your expenses are the biggest factor that will determine how much money you have left over to save. Fixed expenses like rent, utilities, and loans are often unavoidable, but you can save money on other expenses like food, entertainment, and transportation.

- Financial Goals: Your financial goals will also play a role in determining your savings rate. If you are saving for retirement, a down payment on a house, or a large purchase, you will need to save more than if you are just saving for a rainy day.

Tips for increasing your savings rate

- Reduce your expenses: Look for areas where you can cut back on your spending. This could include eating out less, finding cheaper alternatives for entertainment, or negotiating lower rates for your utilities.

- Increase your income: If you can’t cut your expenses, you might need to find ways to increase your income. This could include getting a raise, asking for a promotion, or starting a side hustle.

- Automate your savings: Set up automatic transfers from your checking account to your savings account on a regular basis. This will make it easier to save money without having to think about it.

Common savings goals

- Emergency fund: An emergency fund is a crucial part of any financial plan. It should cover 3-6 months of essential expenses, such as rent, utilities, and food. This fund can help you cover unexpected expenses like medical bills, job loss, or car repairs.

- Retirement savings: If you are saving for retirement, you will need to save a significant amount of money over time. Many financial experts recommend saving at least 15% of your income for retirement.

- Down payment on a house: Saving for a down payment on a house can be a long-term goal. The amount you will need to save will depend on the price of the house and the loan terms.

- Large purchases: You may need to save for large purchases, such as a car, a vacation, or a new appliance. It is important to set a budget and track your progress towards your goal.

How to track your savings progress

- Use a budget: A budget will help you track your income and expenses, so you can see where your money is going. This will make it easier to identify areas where you can cut back on spending and save more.

- Use a savings tracker: A savings tracker can help you stay on track with your savings goals. This can be a simple spreadsheet, or you can use a budgeting app or website.

- Review your savings regularly: It is important to review your savings progress regularly to make sure you are on track. You can also use this time to adjust your budget or savings goals as needed.

What is a realistic yearly savings goal?

There is no one-size-fits-all answer to this question, as a realistic savings goal depends on a number of factors, including your income, expenses, financial goals, and risk tolerance. However, a good starting point is to aim to save at least 10% of your gross income each year.

Factors to Consider When Setting a Savings Goal

- Your income and expenses: The amount you can save will depend on your income and your expenses. If you have a high income and low expenses, you will be able to save more than someone with a low income and high expenses.

- Your financial goals: What are you saving for? Are you saving for retirement, a down payment on a house, or a vacation? Your financial goals will help you determine how much you need to save.

- Your risk tolerance: How comfortable are you with taking risks with your money? If you are risk-averse, you may want to save more than someone who is willing to take on more risk.

- Your age: The younger you are, the more time you have to save for your financial goals. This means you can save less each year and still reach your goals.

- Your current savings: The amount you already have saved will also affect your savings goal. If you have a significant amount saved, you may not need to save as much each year.

How to Set a Realistic Savings Goal

- Track your income and expenses: The first step to setting a realistic savings goal is to understand your financial situation. Track your income and expenses for a few months to see where your money is going.

- Create a budget: Once you know where your money is going, you can create a budget. A budget will help you allocate your income to your various expenses, including savings.

- Set a savings goal: Once you have a budget in place, you can set a savings goal. Start with a small goal and gradually increase it as you become more comfortable saving.

- Automate your savings: The easiest way to save is to automate it. Set up a regular transfer from your checking account to your savings account. This will help you save consistently without having to think about it.

The Benefits of Saving

- Financial security: Saving money provides financial security. It can help you weather unexpected expenses, such as medical bills or job loss.

- Achieve your financial goals: Saving money is essential for achieving your financial goals, such as buying a house, retiring comfortably, or paying for your children’s education.

- Peace of mind: Knowing that you have money saved can provide peace of mind. It can reduce stress and anxiety about your finances.

- Build wealth: Saving money is a key component of building wealth. Over time, your savings can grow significantly through compound interest.

Tips for Saving More Money

- Reduce your expenses: Look for ways to reduce your expenses, such as cutting back on entertainment, eating out less, or finding cheaper alternatives for everyday goods.

- Increase your income: Look for ways to increase your income, such as asking for a raise, getting a side hustle, or selling unwanted items.

- Negotiate bills: Don’t be afraid to negotiate your bills, such as your cable, internet, or phone bill.

- Shop around for better deals: Before you buy anything, shop around to find the best deals.

- Take advantage of free resources: There are many free resources available to help you save money, such as budgeting apps, financial planning websites, and community resources.

How do you set income goals?

Define Your «Why»

Before setting any income goals, you need to understand your motivations. Why do you want to earn more money? Is it for financial security, to pay off debt, to travel, to start a business, or for something else entirely? Having a clear «why» will keep you motivated and focused on your goals.

- Financial security: This might involve building an emergency fund, covering basic expenses, or ensuring financial stability for the future.

- Paying off debt: This could include paying off student loans, credit card debt, or any other outstanding loans.

- Travel: You might want to save up for a dream vacation, explore new cultures, or simply take more trips.

- Starting a business: This might involve saving for a down payment, funding initial operations, or investing in marketing.

- Other personal goals: This could include purchasing a home, investing in your education, or giving back to your community.

Assess Your Current Financial Situation

To set realistic income goals, you need to know where you stand financially. This includes understanding your current income, expenses, assets, and debts. By analyzing your current financial situation, you can identify areas for improvement and set attainable goals.

- Income: This includes your salary, any additional income sources, and potential for growth.

- Expenses: This includes your fixed and variable expenses, such as rent, utilities, food, and transportation.

- Assets: This includes your savings, investments, and any other valuable possessions.

- Debts: This includes all your outstanding loans, credit card balances, and any other debts.

Set SMART Goals

Once you have a clear understanding of your «why» and your current financial situation, you can start setting SMART goals. SMART goals are specific, measurable, achievable, relevant, and time-bound.

- Specific: Define your goal clearly and avoid vagueness.

- Measurable: Ensure you can track your progress toward your goal.

- Achievable: Set goals that are challenging but realistic based on your current situation.

- Relevant: Ensure your goals align with your overall financial objectives and «why».

- Time-bound: Set a specific deadline for achieving your goal to create a sense of urgency.

Break Down Your Goals

Large goals can seem overwhelming, so it’s helpful to break them down into smaller, more manageable steps. This makes the process less daunting and provides a sense of accomplishment as you achieve each milestone.

- Short-term goals: These are smaller goals that can be achieved within a few months or a year.

- Long-term goals: These are larger goals that might take several years to achieve.

Review and Adjust Your Goals Regularly

Your financial situation and goals can change over time. It’s essential to review and adjust your goals regularly to ensure they remain relevant and achievable. You might need to increase or decrease your target income, adjust your timeline, or even redefine your goals altogether. Regularly assessing your progress and making necessary adjustments is crucial for staying on track and achieving your financial aspirations.

Frequently Asked Questions

What does it mean to set realistic savings goals?

Setting realistic savings goals means creating financial targets that are achievable given your current income and expenses. This involves considering your individual circumstances, including your monthly income, fixed expenses (such as rent or mortgage payments), and discretionary spending. It’s about finding a balance between saving for the future and enjoying your current lifestyle. When your goals are realistic, you’re more likely to stick to your savings plan and experience the satisfaction of reaching your financial targets.

How do I calculate how much I can realistically save?

To determine how much you can realistically save, start by tracking your income and expenses for a few months. This will give you a clear picture of your monthly cash flow. Then, subtract your essential expenses (housing, utilities, groceries, transportation) from your total income to arrive at your discretionary income. From your discretionary income, determine a percentage you can allocate to saving. It’s a good idea to start with a small percentage, such as 5% or 10%, and gradually increase it as you get comfortable.

What are some common savings goals for different income levels?

While saving goals will vary based on individual circumstances, here are some general examples:

Low-income earners (under $35,000 annually): Aim to save at least 5% of your income each month. This could be used for an emergency fund or to build a small savings cushion.

Middle-income earners ($35,000 – $100,000 annually): Aim to save 10% to 15% of your income each month. This could be used for retirement, a down payment on a house, or a major purchase.

High-income earners (over $100,000 annually): You may be able to save a higher percentage, such as 20% or more, and can consider investing in a diversified portfolio for long-term wealth building.

What if I can’t save as much as I’d like?

It’s important to be honest with yourself about your current financial situation and adjust your savings goals accordingly. If you’re struggling to save, consider making small changes to your budget, such as reducing your entertainment spending or finding ways to lower your monthly expenses. You can also explore ways to increase your income, such as looking for a side hustle or asking for a raise at work. Remember that even small savings add up over time.