Investing is a journey, not a sprint. While the allure of quick, substantial returns is tempting, setting realistic expectations for your portfolio is crucial for long-term success. This article will delve into the practical steps for establishing a grounded outlook, taking into account factors like your investment horizon, risk tolerance, and market conditions. By understanding these elements and aligning your expectations accordingly, you can navigate the investment landscape with a clear vision and a strategy that aligns with your financial goals.

Understanding Realistic Return Expectations for Your Portfolio

Understand the Basics of Investing

Investing is about balancing risk and reward. The higher the potential return, the higher the risk. Understanding this relationship is crucial to setting realistic expectations.

| Risk | Return Potential |

|---|---|

| Low | Low |

| Medium | Medium |

| High | High |

Consider Your Time Horizon

The longer your investment horizon, the more time you have for your investments to grow. This allows you to take on more risk and potentially earn higher returns.

| Time Horizon | Return Expectation |

|---|---|

| Short-term (1-3 years) | Lower |

| Medium-term (3-5 years) | Moderate |

| Long-term (5+ years) | Higher |

Factor in Inflation

Inflation erodes the purchasing power of your money, so you need to consider its impact on your investment returns. To maintain your purchasing power, your investments should grow at least as fast as inflation.

| Inflation Rate | Real Return |

|---|---|

| 2% | 5% – 2% = 3% |

| 3% | 8% – 3% = 5% |

| 4% | 10% – 4% = 6% |

Research Historical Returns

Looking at historical market data can give you an idea of what to expect from different asset classes. Remember that past performance is not indicative of future results, but it can offer valuable insights.

| Asset Class | Average Historical Return (annualized) |

|---|---|

| US Stocks (S&P 500) | 10% |

| Bonds | 5% |

| Real Estate | 8% |

Don’t Chase High Returns

Chasing high returns often leads to risky investments that can result in significant losses. Focus on building a diversified portfolio that aligns with your risk tolerance and time horizon.

| Investment Strategy | Risk | Return Potential |

|---|---|---|

| High-growth stocks | High | High |

| Index funds | Low | Moderate |

| Bonds | Low | Low |

Is 7% return on investment realistic?

Is 7% Return on Investment Realistic?

A 7% return on investment (ROI) is considered realistic but not guaranteed, as it depends on several factors, including the specific investment, market conditions, and the investor’s risk tolerance. To determine if a 7% ROI is achievable, you should consider the following:

Factors Affecting ROI

- Investment Type: Different investment types carry varying levels of risk and potential returns. For instance, stocks tend to have higher potential returns but also higher volatility compared to bonds, which are generally considered safer but offer lower returns.

- Market Conditions: The overall economic and market conditions can significantly impact investment performance. During periods of economic growth and positive market sentiment, investments are more likely to generate higher returns. Conversely, during economic downturns or market volatility, returns may be lower or even negative.

- Investment Strategy: The chosen investment strategy plays a crucial role in determining the potential ROI. Investors with a long-term investment horizon and a diversified portfolio, for example, are likely to achieve higher returns over time compared to those with a short-term investment horizon or a concentrated portfolio.

- Risk Tolerance: An investor’s risk tolerance is essential. Higher risk tolerance allows for potentially higher returns, while lower risk tolerance often translates to lower returns.

- Time Horizon: Investment returns often compound over time. A longer investment horizon allows for more time for investments to grow, potentially leading to higher returns.

Historical Returns

Historically, the S&P 500 index has generated an average annual return of around 10%, including dividends, over the long term. However, this does not guarantee future returns, and there are periods where the market has experienced significant losses.

Inflation and Real Returns

It’s important to consider the impact of inflation when evaluating ROI. A 7% return may not be sufficient to outpace inflation, particularly in periods of high inflation. To achieve a real return, which is the return after accounting for inflation, you need to earn a return higher than the inflation rate. For example, if inflation is running at 3%, you would need a return of at least 10% to achieve a real return of 7%.

Diversification and Asset Allocation

A diversified portfolio that includes a mix of different asset classes, such as stocks, bonds, real estate, and commodities, can help mitigate risk and potentially achieve a target ROI. Asset allocation, which refers to the distribution of investments across different asset classes, plays a crucial role in portfolio diversification. An appropriate asset allocation strategy should be tailored to an investor’s specific risk tolerance and investment goals.

Is a 12% return realistic?

The question of whether a 12% return is realistic depends heavily on the context. Here’s a breakdown of factors to consider:

Investment Type

Stocks: Historically, the S&P 500 has returned an average of about 10% per year over the long term. However, this is an average, and individual years can be much higher or lower. 12% is possible in the stock market, but it’s not guaranteed and comes with significant risk.

Bonds: Bonds generally offer lower returns than stocks but are also less risky. A 12% return on bonds is highly unlikely, especially in today’s low-interest-rate environment.

Real Estate: Real estate returns can vary widely depending on location, market conditions, and the type of property. While 12% returns are possible, they require careful selection and active management.

Alternative Investments: Hedge funds, private equity, and other alternative investments can potentially generate high returns, but they often come with significant risk and illiquidity.

Time Horizon

Short-Term: A 12% return over a short period (e.g., a year) is possible but unlikely to be sustained. Market fluctuations and unforeseen events can easily derail short-term investment goals.

Long-Term: A 12% return over a long period (e.g., 10+ years) is more achievable, especially with a diversified portfolio of stocks and other assets.

Investment Strategy

Passive Investing: Index funds and ETFs offer low-cost, diversified exposure to the market, typically targeting market-average returns. Achieving a 12% return through passive investing might require taking on additional risk.

Active Investing: Active management involves picking individual stocks or using strategies to try to outperform the market. While a 12% return is possible with active investing, it requires skill, experience, and a strong understanding of market dynamics.

Risk Tolerance

High Risk Tolerance: Investors with a high risk tolerance may be willing to accept greater volatility in pursuit of higher returns, making a 12% return more achievable.

Low Risk Tolerance: Investors with a low risk tolerance may prioritize preservation of capital over high returns. A 12% return might be deemed too risky for such investors.

Current Market Conditions

Economic Growth: A strong economy typically leads to higher stock market returns, making a 12% return more likely.

Interest Rates: Low interest rates can make it more challenging to earn high returns, as bond yields are typically lower.

Inflation: High inflation erodes the purchasing power of returns, making it important to consider the real return (adjusted for inflation).

How to calculate the expected return of a portfolio?

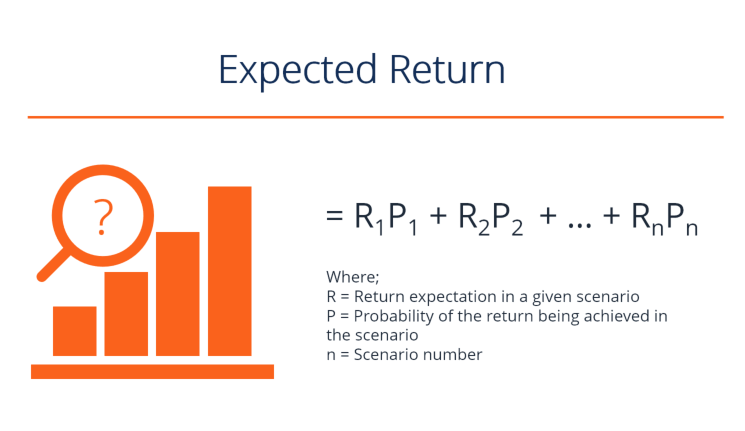

What is Expected Return?

The expected return of a portfolio is the anticipated rate of return that an investor expects to earn from their investment. It’s a key factor in investment decision-making, as it helps investors gauge the potential profitability of their portfolio.

How to Calculate Expected Return

The expected return of a portfolio is calculated as the weighted average of the expected returns of each asset in the portfolio. The weights represent the proportion of the portfolio’s total value that is allocated to each asset.

- Determine the Expected Return for Each Asset: This can be based on historical data, market analysis, or analysts’ forecasts. For example, you might use the average historical return of a particular stock as an estimate of its future expected return.

- Determine the Weight of Each Asset: This is the proportion of the total portfolio value that is allocated to each asset. For example, if you have a $10,000 portfolio and $2,000 is invested in stock A, the weight of stock A is 20% (2,000/10,000).

- Multiply the Expected Return of Each Asset by its Weight: This will give you the contribution of each asset to the overall expected return of the portfolio.

- Sum up the Contributions of Each Asset: This will give you the total expected return of the portfolio.

Example:

Let’s say you have a portfolio with two assets: Stock A and Bond B.

- Expected Return of Stock A: 10%

- Expected Return of Bond B: 5%

- Weight of Stock A: 60%

- Weight of Bond B: 40%

To calculate the expected return of the portfolio, you would do the following:

Expected Return of Portfolio = (Expected Return of Stock A Weight of Stock A) + (Expected Return of Bond B Weight of Bond B)

Expected Return of Portfolio = (10% 60%) + (5% 40%) = 8%

Factors Affecting Expected Return

There are several factors that can affect the expected return of a portfolio, including:

- Market Conditions: Overall economic growth, interest rates, and inflation can all impact asset prices and, consequently, expected returns.

- Risk Tolerance: Investors with a higher risk tolerance may be willing to invest in assets with higher expected returns but also higher risk.

- Investment Strategy: Different investment strategies, such as value investing or growth investing, can lead to different expected returns.

- Diversification: Diversifying your portfolio across different asset classes can help to reduce overall risk and improve expected returns.

Limitations of Expected Return

It’s important to note that expected return is just an estimate, and there is no guarantee that the actual return will match the expected return.

- Past Performance is Not Indicative of Future Results: Historical returns are not necessarily indicative of future returns. Market conditions can change unexpectedly, leading to deviations from expected returns.

- Unforeseen Events: Unexpected events, such as economic crises or political instability, can significantly impact asset prices and expected returns.

What is a realistic portfolio return?

A realistic portfolio return is the expected rate of return on your investments over a specific period of time. It’s important to consider several factors when determining a realistic portfolio return, such as your investment goals, risk tolerance, and time horizon. Keep in mind that past performance is not indicative of future results, and there are no guarantees in investing. However, a realistic return can be a good starting point for financial planning and investment decisions.

Factors influencing portfolio return

Several factors influence your portfolio’s expected return. These include:

- Market conditions: Stock market performance, interest rates, and inflation play a significant role in portfolio returns.

- Investment strategy: Your asset allocation, investment choices, and diversification strategy directly impact expected returns.

- Risk tolerance: The higher the risk you’re willing to take, the higher the potential return, but also the higher the potential for loss.

- Time horizon: The longer your investment horizon, the more time you have for your investments to recover from market fluctuations, potentially leading to higher returns.

- Investment fees: Fees associated with your investments, such as management fees or trading commissions, can eat into your potential returns.

Historical returns

While past performance isn’t a guarantee of future results, examining historical returns can provide insights into potential returns. Over the long term, the S&P 500 index has averaged an annual return of approximately 10%. However, it’s crucial to remember that this is an average, and returns can vary significantly from year to year.

Realistic expectations

Setting realistic expectations for portfolio returns is essential. It’s crucial to avoid unrealistic or overly optimistic projections. A realistic return should be achievable while balancing risk and potential rewards. Consider a range of returns rather than a single number, allowing for market volatility and unforeseen circumstances.

How to calculate realistic return

Determining a realistic return involves several steps:

- Define your investment goals: Identify your financial objectives, such as retirement savings, buying a house, or funding your children’s education.

- Assess your risk tolerance: Determine your comfort level with investment risk and how much volatility you can handle.

- Consider your time horizon: Understand how long you’ll be investing and how much time you have for your investments to grow.

- Research historical market returns: Examine historical performance data for different asset classes and investment strategies.

- Seek professional advice: Consult with a financial advisor to discuss your specific circumstances and obtain personalized recommendations.

Frequently Asked Questions

What are realistic return expectations for my portfolio?

There is no single answer to this question, as realistic return expectations will vary depending on a number of factors, including your investment goals, risk tolerance, time horizon, and the current market conditions. However, it is important to set realistic expectations that are based on historical data and current market trends.

A good starting point is to consider the average historical returns of different asset classes. For example, the S&P 500 index has historically returned an average of about 10% per year over the long term. However, it is important to note that this is just an average, and actual returns can vary significantly from year to year. In recent years, for example, the S&P 500 has experienced periods of both strong growth and significant decline.

Another important factor to consider is your risk tolerance. If you are comfortable with a higher level of risk, you may be willing to accept a higher potential return. However, you should also be prepared for the possibility of greater losses. If you are more risk-averse, you may prefer to invest in lower-risk assets, even if this means accepting a lower potential return.

Finally, it is important to consider your time horizon. If you are investing for the long term, you have more time to recover from any short-term market fluctuations. This means that you can afford to take on more risk and potentially earn higher returns. However, if you need to access your money in the short term, you may need to be more conservative with your investments.

How can I calculate realistic return expectations for my portfolio?

There are a number of different ways to calculate realistic return expectations for your portfolio. One common method is to use a Monte Carlo simulation. This is a statistical technique that uses random numbers to generate a large number of possible future scenarios. By running the simulation many times, you can get a sense of the range of possible returns that your portfolio could generate over time.

Another approach is to use a backtesting model. This involves looking at historical data to see how different asset classes have performed in the past. By analyzing historical data, you can get a sense of the average returns that you can expect from different investments.

It is important to note that both Monte Carlo simulations and backtesting models are based on historical data, which may not be a perfect predictor of future performance. It is also important to keep in mind that market conditions can change rapidly, which can affect your portfolio’s performance.

What are some common mistakes to avoid when setting return expectations?

There are a number of common mistakes that investors make when setting return expectations. One common mistake is to overestimate returns. This can lead to disappointment and even financial hardship if your investments do not perform as well as you expected.

Another common mistake is to underestimate risk. This can lead to taking on more risk than you are comfortable with, which can increase the likelihood of losses.

It is also important to avoid chasing returns. This means investing in assets that are currently performing well, but may not be a good long-term investment.

Finally, it is important to be patient. Investing is a long-term game, and it is important to be realistic about the time it takes to build wealth. Do not expect to get rich quickly, and do not be discouraged by short-term market fluctuations.

What should I do if my portfolio is not meeting my return expectations?

If your portfolio is not meeting your return expectations, there are a few things you can do. First, it is important to review your investment strategy and make sure that it is still appropriate for your goals and risk tolerance. You may need to adjust your asset allocation or choose different investments.

Second, it is important to understand the reasons why your portfolio is not performing as well as you expected. This may be due to market conditions, your investment choices, or a combination of factors.

Third, it is important to be patient. Market conditions can change rapidly, and it is important to remember that investing is a long-term game. Do not make any rash decisions based on short-term market fluctuations.

Finally, it is important to seek professional advice if you are not comfortable managing your own investments. A financial advisor can help you develop a personalized investment strategy that meets your needs.