Here’s a possible introduction for an article on «How to Plan for Annual Budget Goals»:

***

Achieving financial goals can be a daunting task, but it doesn’t have to be. With a well-crafted plan, you can transform your financial aspirations into reality. This article will equip you with the essential tools and strategies to set and achieve your annual budget goals. From understanding your current financial situation to setting realistic targets and developing a step-by-step plan, we’ll guide you through the process of budgeting for a successful year. Let’s embark on this journey toward financial stability and fulfillment.

***

How to Plan for Annual Budget Goals

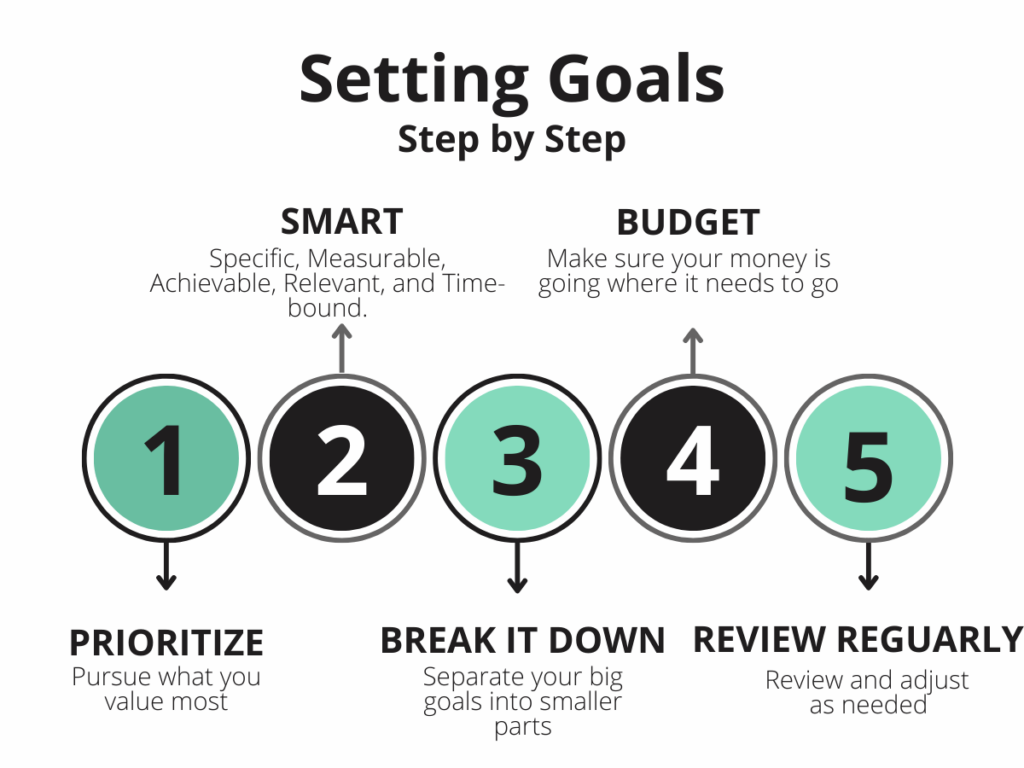

1. Set Realistic Goals

When setting financial goals, it is crucial to be realistic. Avoid aiming for unattainable targets, as it can lead to frustration and discouragement. Consider your current financial situation, income, and expenses to determine what is achievable within a year. It’s also important to break down your goals into smaller, more manageable steps. For example, instead of aiming to save $10,000 in a year, you can set a monthly goal of saving $833. This approach makes the process feel less overwhelming and more achievable.

2. Track Your Spending

Before you can start planning for your budget goals, you need to understand where your money is going. Tracking your spending allows you to identify areas where you can cut back and allocate funds towards your financial goals. There are various methods to track spending, such as using a budgeting app, spreadsheets, or simply keeping a journal. Consistent tracking is essential for identifying spending patterns and making informed decisions about your budget.

3. Create a Budget

Once you have a clear picture of your spending habits, it’s time to create a budget. This involves outlining your income and expenses, allocating funds to different categories, and ensuring you have a surplus to contribute towards your goals. A budget helps you prioritize spending and stay on track. It provides a framework for making financial decisions and ensures that you are allocating your money effectively.

4. Automate Your Savings

Automating your savings is a crucial step in achieving your financial goals. By setting up automatic transfers from your checking account to your savings account, you ensure consistent contributions towards your goals. This approach removes the temptation to spend the money and allows you to build a solid foundation for your financial future. Consider automating your savings at the beginning of the month, so you’re not relying on your remaining balance to make contributions.

5. Review and Adjust Regularly

Your financial situation and goals can change over time, so it’s essential to review and adjust your budget regularly. Regularly reviewing your budget helps you identify any areas where you can make adjustments to better align with your goals. For example, you may need to reduce expenses or increase your income to stay on track. It’s also important to celebrate your progress and acknowledge your accomplishments along the way. This keeps you motivated and encourages you to stay committed to your goals.

How to prepare an annual budget plan?

Gather Your Financial Information

To create an accurate budget, you need to know where your money is coming from and where it’s going. Gather all your income and expense information. This may include:

- Pay stubs or W-2 forms for income sources.

- Bank statements to track deposits, withdrawals, and recurring payments.

- Credit card statements to monitor purchases and interest rates.

- Utility bills for electricity, gas, water, and internet.

- Other expense receipts for groceries, entertainment, transportation, and subscriptions.

Set Your Financial Goals

It’s important to have a clear idea of what you want to achieve financially. What are your priorities? Do you want to pay off debt, save for retirement, buy a house, or travel? Your goals will guide your budget.

- Short-term goals (within a year) might include paying off a credit card balance or saving for a vacation.

- Long-term goals (over a year) could be saving for retirement, buying a home, or funding your child’s education.

- Set specific, measurable, achievable, relevant, and time-bound (SMART) goals to keep you motivated and on track.

Track Your Spending

Once you’ve gathered your financial information, it’s time to track your spending. You can use a budgeting app, spreadsheet, or even a simple notebook to record your expenses. This will help you identify areas where you can cut back.

- Categorize your expenses by type, such as housing, food, transportation, and entertainment. This will provide insights into spending habits.

- Analyze your spending patterns to spot recurring costs and identify areas for potential savings.

- Use a budgeting tool to automate the process and generate helpful reports.

Allocate Your Income

Now that you have a good understanding of your income and expenses, it’s time to allocate your income. This means deciding how much money you’ll spend on each category. It’s helpful to use the 50/30/20 budget rule as a guideline.

- 50% for needs: This includes essential expenses like housing, utilities, food, transportation, and healthcare.

- 30% for wants: This covers discretionary spending like entertainment, dining out, travel, and hobbies.

- 20% for savings and debt repayment: This is crucial for building your financial security and reaching your goals.

Review and Adjust Your Budget

Your budget shouldn’t be set in stone. Regularly review your budget and make adjustments as needed. Life changes, and your financial circumstances may also evolve.

- Review your budget monthly or quarterly to ensure it aligns with your goals and spending habits.

- Adjust your budget if necessary. This could involve cutting back on expenses, increasing income, or making changes to your goals.

- Stay flexible and adaptable to your evolving needs and financial situation.

What is the 50/30/20 budget rule?

The 50/30/20 budget rule is a simple and effective budgeting method that divides your after-tax income into three categories: needs, wants, and savings. The rule suggests allocating:

50% of your income to needs: These are essential expenses like rent, utilities, groceries, transportation, and healthcare.

30% of your income to wants: These are discretionary expenses like entertainment, dining out, shopping, and travel.

20% of your income to savings and debt repayment: This category includes paying off debt, building an emergency fund, saving for retirement, and other financial goals.

Benefits of the 50/30/20 Budget Rule

The 50/30/20 rule offers several benefits for managing your finances:

- Simplifies budgeting: This method breaks down your income into clear categories, making it easier to track your spending and ensure you’re allocating money effectively.

- Encourages saving: By allocating 20% of your income to savings, you automatically prioritize financial goals and build financial security.

- Provides flexibility: The 50/30/20 rule allows for some flexibility in adjusting the percentages based on your individual needs and priorities.

- Promotes financial discipline: By consciously allocating your income, you develop better spending habits and avoid overspending.

- Improves financial well-being: This method helps you take control of your finances, reduce debt, and achieve your financial goals.

How to Implement the 50/30/20 Budget Rule

To start using the 50/30/20 budget rule, follow these steps:

- Calculate your net income: Determine your income after taxes and other deductions.

- Track your expenses: Analyze your spending habits for a month or two to understand where your money is going.

- Allocate your income: Divide your net income into the three categories (50% needs, 30% wants, 20% savings) and adjust as needed.

- Set financial goals: Define your short-term and long-term financial goals, such as paying off debt, building an emergency fund, or saving for retirement.

- Review and adjust your budget: Regularly review your budget and make adjustments as your needs and priorities change.

Tips for Using the 50/30/20 Budget Rule

Here are some tips to make the most of the 50/30/20 budget rule:

- Prioritize needs: Ensure that your essential expenses are covered first before allocating money to wants or savings.

- Be realistic with your wants: Set reasonable limits on your discretionary spending and look for ways to cut back if needed.

- Automate savings: Set up automatic transfers to your savings account to ensure you are consistently saving.

- Track your progress: Regularly monitor your spending and savings to see if you’re on track with your budget.

- Seek professional help: If you’re struggling to implement or maintain the 50/30/20 budget rule, consider seeking guidance from a financial advisor.

Common Misconceptions about the 50/30/20 Budget Rule

There are some common misconceptions about the 50/30/20 budget rule that are important to address:

- It’s not a one-size-fits-all solution: The 50/30/20 rule is a guideline and may need to be adjusted based on individual circumstances and financial goals. It’s important to find a budget that works for you.

- It doesn’t dictate specific amounts: The percentages are a starting point, and the actual amounts will vary depending on your income level. Focus on allocating your income effectively rather than adhering strictly to the percentages.

- It’s not a quick fix: Implementing the 50/30/20 budget rule requires discipline and effort, but it can lead to long-term financial stability and well-being.

How to plan a budget for the year?

Track Your Spending

The first step to creating a budget is to know where your money is going. Track your spending for a month or two, using a budgeting app, spreadsheet, or notebook. This will give you a clear picture of your income and expenses.

- Use a budgeting app: There are many budgeting apps available, such as Mint, Personal Capital, and YNAB (You Need a Budget). These apps can automatically track your spending and categorize your transactions.

- Create a spreadsheet: If you prefer a more hands-on approach, you can create a simple spreadsheet to track your income and expenses.

- Use a notebook: If you’re old school, you can use a notebook to track your spending.

Set Financial Goals

Before you can start budgeting, you need to have some financial goals in mind. What do you want to achieve with your money? Do you want to pay off debt, save for a down payment on a house, or retire early?

- Short-term goals: These are goals that you want to achieve within a year, such as paying off credit card debt or saving for a vacation.

- Long-term goals: These are goals that you want to achieve in the future, such as retiring early or buying a house.

Create a Budget

Once you know where your money is going and what your financial goals are, you can start creating a budget. A budget is simply a plan for how you will spend your money.

- List your income: Start by listing all of your sources of income, such as your salary, wages, and any other income you receive.

- List your expenses: Next, list all of your expenses, such as housing, food, transportation, and entertainment.

- Categorize your expenses: Once you have listed all of your expenses, categorize them into different groups, such as housing, food, transportation, and entertainment.

- Allocate your income: Now that you have a list of your income and expenses, allocate your income to each category.

Review and Adjust Your Budget

Your budget is not set in stone. It’s important to review your budget regularly and make adjustments as needed.

- Review your budget monthly: Review your budget at least once a month to make sure you’re on track to meet your financial goals.

- Adjust your budget as needed: If you find that you’re not meeting your financial goals, adjust your budget accordingly. For example, if you’re spending too much on entertainment, you may need to cut back on your spending in that category.

Stick to Your Budget

The most important step to creating a successful budget is sticking to it.

- Use cash or a debit card: Paying with cash or a debit card can help you stay within your budget, as you’ll only be able to spend what you have.

- Avoid using credit cards: Credit cards can lead to overspending and debt.

- Track your spending regularly: Track your spending regularly to make sure you’re staying within your budget.

How do you set budget goals?

Setting budget goals is essential for achieving financial stability and reaching your financial aspirations. Here’s a detailed breakdown of how to establish effective budget goals:

1. Define your financial objectives.

What do you want to achieve with your budget? This could be anything from saving for retirement, paying off debt, or buying a house.

Identify your short-term and long-term goals. This helps prioritize your spending and allocate funds accordingly.

Be specific and measurable. Instead of saying «save money,» set a goal like «save $5,000 for a down payment on a car within 12 months.»

Make your goals realistic and achievable. Avoid setting unrealistic goals that will only lead to disappointment.

2. Analyze your current spending habits.

Before you can set goals, you need to understand where your money is going.

Track your expenses for at least one month. Use a budgeting app, spreadsheet, or simply a notebook.

Categorize your expenses. Identify where you are spending the most, such as housing, transportation, food, or entertainment.

Identify areas where you can cut back. Are there expenses you can reduce or eliminate?

3. Create a realistic budget.

Once you understand your spending habits, you can create a budget that aligns with your financial goals.

Allocate funds to each expense category. Base this on your priorities and desired spending levels.

Set aside funds for savings and debt repayment. Prioritize these goals in your budget.

Be flexible and adjust your budget as needed. Your circumstances may change over time, so be prepared to adapt your budget.

4. Set specific and measurable goals.

Vague goals are less likely to be achieved.

Set clear targets for each of your financial objectives. For example, «save $1,000 per month for retirement» or «pay off $500 in credit card debt each month.»

Create a timeline for each goal. This will help you stay on track and track your progress.

Break down large goals into smaller milestones. This can make them seem more manageable and less daunting.

5. Monitor your progress and adjust as needed.

Tracking your progress is key to ensuring your budget is working.

Review your budget regularly. At least once a month, assess your spending against your goals.

Make adjustments as needed. Your financial situation may change, so it’s essential to adapt your budget accordingly.

Celebrate your achievements. This will help you stay motivated and maintain momentum.

Frequently Asked Questions

What are the benefits of creating a budget plan?

A budget plan offers numerous advantages, including:

- Financial Clarity: It provides a comprehensive overview of your income and expenses, allowing you to understand your financial situation better.

- Financial Control: By tracking your spending, you can identify areas where you can cut back and make smarter financial decisions.

- Goal Achievement: Budgeting helps you prioritize your financial goals and allocate resources towards achieving them effectively.

- Reduced Stress: Knowing your finances are under control can significantly reduce financial anxiety and stress.

- Increased Savings: By monitoring your spending and identifying areas for savings, you can accumulate wealth over time.

How do I create an annual budget plan?

Creating a budget plan involves several steps:

- Track Your Income: List all sources of income, including salary, investments, and other regular earnings.

- Track Your Expenses: Categorize your expenses, such as housing, utilities, transportation, food, entertainment, and debt payments.

- Estimate Future Income and Expenses: Project your income and expenses for the upcoming year, considering any potential changes or increases.

- Set Financial Goals: Define your short-term and long-term financial objectives, such as saving for a house, paying off debt, or investing for retirement.

- Allocate Your Budget: Based on your goals and projected expenses, allocate your income to different categories. It’s crucial to prioritize essential expenses and allocate funds for savings and debt repayment.

- Review and Adjust Regularly: Regularly review your budget plan and make adjustments as needed to ensure it aligns with your changing financial situation and goals.

What are some common budgeting methods?

There are various popular budgeting methods, each with its own approach:

- 50/30/20 Budget: This method allocates 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment.

- Zero-Based Budgeting: This approach involves allocating every dollar of your income to specific categories, leaving no room for unplanned spending.

- Envelope System: This method involves physically allocating cash for different spending categories into separate envelopes.

- Pay Yourself First: This strategy encourages saving a predetermined amount of money before paying other expenses.

It’s crucial to choose a method that aligns with your financial personality and goals.

What are some tips for sticking to my budget?

Sticking to your budget requires discipline and consistency. Here are some helpful tips:

- Set Realistic Goals: Avoid setting overly ambitious goals that you’re unlikely to achieve. Start small and gradually increase your savings or spending reductions.

- Automate Savings: Set up automatic transfers from your checking account to your savings account to ensure regular savings.

- Track Your Expenses: Regularly monitor your spending and compare it to your budget. This helps you identify areas for improvement.

- Limit Impulse Purchases: Avoid making unnecessary purchases or spending on things you don’t truly need. Consider the long-term implications of your spending decisions.

- Seek Support: Share your budgeting goals with friends, family, or a financial advisor for accountability and encouragement.