Credit card debt can feel like a suffocating weight, threatening to derail your dreams and ambitions. It’s easy to fall into the trap of overspending, but the repercussions can be severe. However, you don’t have to sacrifice your lifestyle to overcome this financial burden. This article explores practical strategies for effectively managing credit card debt without compromising on the things you enjoy. From budgeting techniques to debt consolidation and negotiating with creditors, we’ll delve into actionable steps you can take to regain control of your finances and reclaim your financial freedom.

Claro, aquí tienes un subtítulo H2 y 5 subtítulos H3 con información detallada sobre cómo gestionar la deuda de las tarjetas de crédito sin sacrificar tu estilo de vida, así como una tabla en HTML que contiene los puntos clave.

How to Manage Credit Card Debt Without Sacrificing Your Lifestyle

1. Create a Budget and Track Your Spending

A budget is a crucial tool for managing credit card debt because it helps you identify where your money is going and where you can cut back. Tracking your spending can be done through budgeting apps, spreadsheets, or even a simple notebook.

Here are some tips for creating a budget:

List all your monthly income and expenses.

Categorize your expenses (e.g., housing, food, transportation, entertainment).

Track your spending for at least one month to see where your money is going.

Identify areas where you can cut back.

Allocate a specific amount of money to pay down your credit card debt.

Here are some tips for tracking your spending:

Use a budgeting app or spreadsheet.

Keep track of your receipts.

Review your bank statements regularly.

Here are the benefits of creating a budget and tracking your spending:

You can see where your money is going.

You can identify areas where you can cut back.

You can save more money.

You can pay down your credit card debt faster.

| Benefit | Description |

|---|---|

| See where your money is going | A budget helps you understand how you spend your money and identify areas where you can cut back. |

| Identify areas where you can cut back | By tracking your spending, you can see where your money is going and make informed decisions about where to cut back. |

| Save more money | A budget can help you save more money by helping you identify areas where you can cut back and allocate funds towards your savings goals. |

| Pay down your credit card debt faster | By allocating a specific amount of money to pay down your credit card debt each month, you can pay it off faster. |

2. Make a Debt Snowball or Debt Avalanche Plan

A debt snowball involves paying off your smallest debt first, while a debt avalanche involves paying off your highest interest rate debt first. Both methods are effective, but the debt snowball can be more motivating, as you’re quickly paying off debts and getting a sense of accomplishment.

Here are the steps for creating a debt snowball plan:

List your debts from smallest to largest balance.

Make minimum payments on all your debts except for the smallest one.

Pay as much as you can towards the smallest debt.

Once the smallest debt is paid off, roll that payment amount onto the next smallest debt.

Continue this process until all your debts are paid off.

Here are the steps for creating a debt avalanche plan:

List your debts from highest interest rate to lowest interest rate.

Make minimum payments on all your debts except for the highest interest rate debt.

Pay as much as you can towards the highest interest rate debt.

Once the highest interest rate debt is paid off, roll that payment amount onto the next highest interest rate debt.

Continue this process until all your debts are paid off.

Here are the benefits of creating a debt snowball or debt avalanche plan:

You can pay down your debt faster.

You can save money on interest charges.

You can feel more motivated and in control.

| Plan | Description |

|---|---|

| Debt Snowball | Focuses on paying off the smallest debt first, providing a sense of accomplishment and motivation to continue paying off debts. |

| Debt Avalanche | Prioritizes paying off debts with the highest interest rates first, minimizing interest charges and saving money in the long run. |

3. Look for Ways to Increase Your Income

Increasing your income can provide you with more money to pay down your credit card debt.

Here are some ways to increase your income:

Get a second job.

Sell unwanted items.

Start a side hustle.

Ask for a raise at your current job.

Negotiate a better salary at your current job.

Find a new job with a higher salary.

Here are the benefits of increasing your income:

You can pay down your credit card debt faster.

You can save more money.

You can have more financial freedom.

| Method | Description |

|---|---|

| Get a second job | Taking on a second job, even if it’s part-time, can significantly increase your income and allow for faster debt repayment. |

| Sell unwanted items | Selling unwanted items, like clothing, electronics, or furniture, can provide a quick influx of cash. |

| Start a side hustle | Pursuing a side hustle, such as freelance work, tutoring, or crafting, can offer additional income and help pay off debt faster. |

| Ask for a raise | Negotiating a raise at your current job can increase your income and provide more funds for debt repayment. |

| Negotiate a better salary | During salary negotiations, aim for a salary that aligns with your market value and allows for adequate funds to address your debt. |

| Find a new job with a higher salary | Searching for a new job with a higher salary can be a strategic move to increase your income and accelerate debt repayment. |

4. Negotiate with Your Credit Card Company

You may be able to negotiate with your credit card company to lower your interest rate, reduce your minimum payment, or even settle for a lower balance.

Here are some tips for negotiating with your credit card company:

Be polite and respectful.

Be prepared to explain your situation.

Be willing to negotiate.

Have a plan in place for how you will make your payments.

Here are the benefits of negotiating with your credit card company:

You can lower your interest rate.

You can reduce your minimum payment.

You can settle for a lower balance.

| Benefit | Description |

|---|---|

| Lower your interest rate | Negotiating a lower interest rate can significantly reduce the amount of interest you pay over time, freeing up more money for debt repayment. |

| Reduce your minimum payment | Reducing your minimum payment can make it easier to manage your debt and potentially allocate more funds towards principal repayment. |

| Settle for a lower balance | In some cases, credit card companies may be willing to settle for a lower balance, which can reduce your overall debt burden. |

5. Avoid Using Your Credit Cards for Non-Essential Purchases

One of the best ways to manage credit card debt is to avoid using your credit cards for non-essential purchases. This will help you stay on track with your budget and prevent you from accumulating more debt.

Here are some tips for avoiding using your credit cards for non-essential purchases:

Use cash for everyday purchases.

Use a debit card for purchases you can’t afford to pay for in cash.

Set a spending limit for your credit cards.

Track your spending to see where your money is going.

Here are the benefits of avoiding using your credit cards for non-essential purchases:

You can avoid accumulating more debt.

You can stay on track with your budget.

You can have more financial freedom.

| Benefit | Description |

|---|---|

| Avoid accumulating more debt | By using cash or debit cards for non-essential purchases, you can avoid racking up more debt on your credit cards and focus on paying down existing debt. |

| Stay on track with your budget | Avoiding credit card use for non-essential items helps you stick to your budget and prevents overspending. |

| Have more financial freedom | By reducing credit card usage, you can decrease your debt burden and gain more financial freedom. |

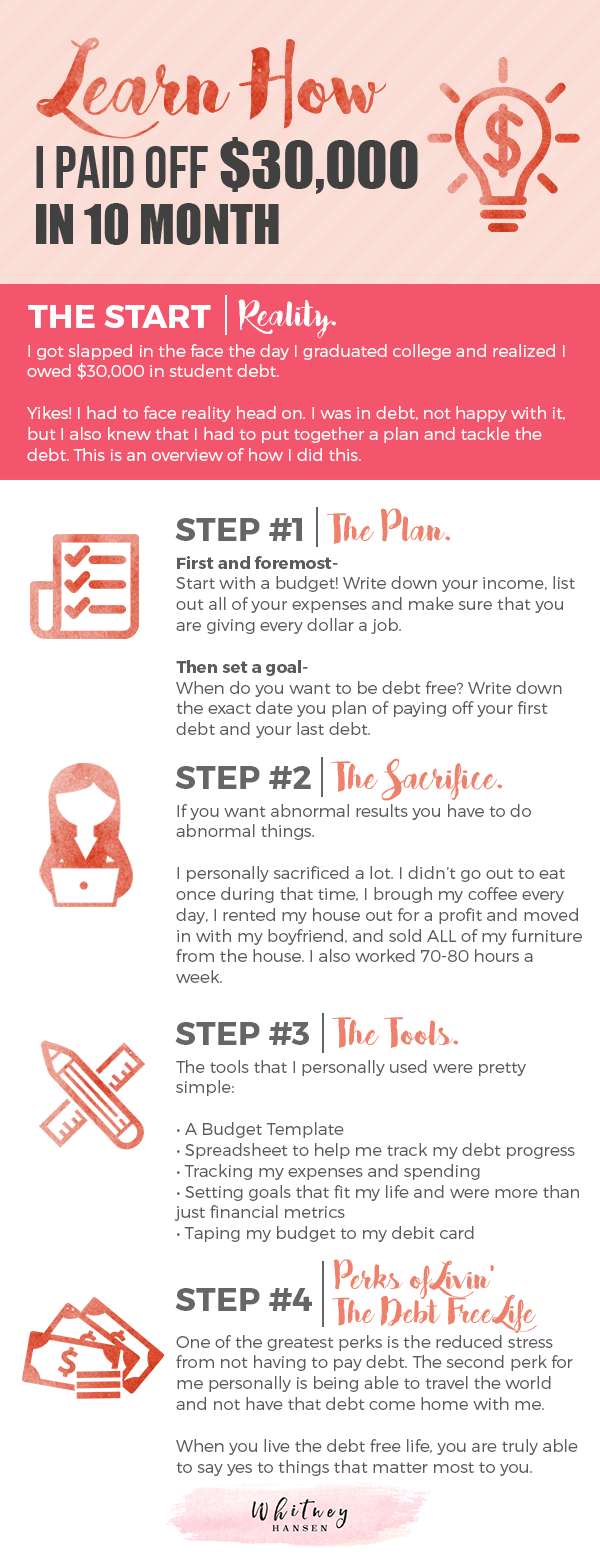

How to pay off $30,000 in credit card debt?

Create a Budget and Track Your Spending

The first step to paying off $30,000 in credit card debt is to understand where your money is going. Create a detailed budget that tracks all of your income and expenses. This will help you identify areas where you can cut back and free up more cash to put towards your debt. Use budgeting apps or a simple spreadsheet to track your spending.

- List all your income sources. This includes your salary, any side gigs, and any other regular income you receive.

- Track your spending. Use a budgeting app, spreadsheet, or notebook to track every dollar you spend. Be sure to include both fixed expenses (like rent, utilities, and car payments) and variable expenses (like groceries, entertainment, and dining out).

- Identify areas where you can cut back. Once you have a clear picture of your spending, look for areas where you can cut back. This might include dining out less often, reducing your entertainment budget, or finding cheaper alternatives to your current expenses.

Consider Debt Consolidation

Debt consolidation can be a helpful strategy for paying off credit card debt. This involves taking out a new loan with a lower interest rate to pay off your existing credit card debt. This can help you reduce your monthly payments and save money on interest.

- Shop around for a low-interest loan. Compare interest rates from different lenders, and consider using a personal loan or a balance transfer credit card.

- Make sure you can afford the new loan payments. Debt consolidation can help you save money, but only if you can afford the monthly payments. Make sure the new loan payments are manageable given your budget.

- Understand the fees associated with debt consolidation. Some debt consolidation loans have origination fees, which can impact the overall cost of the loan.

Negotiate with Your Credit Card Companies

Don’t be afraid to reach out to your credit card companies and negotiate your debt. They may be willing to lower your interest rate, waive late fees, or reduce your balance. They might even be able to offer you a hardship program, which can help you reduce your monthly payments for a set period of time.

- Be polite and professional. When you contact your credit card company, be polite and professional, and explain your situation clearly.

- Have a plan in mind. Before you call, have a plan for how you want to handle your debt, and be prepared to discuss your options with the credit card company representative.

- Be persistent. If you don’t get the results you want on the first try, don’t give up. Be persistent and continue to negotiate until you reach an agreement that works for you.

Focus on Paying More Than the Minimum

The minimum payment on your credit card may be tempting to make, but doing so will only keep you in debt for longer. Instead, aim to pay more than the minimum payment each month. This will help you pay off your debt faster and save money on interest.

- Set a goal for your extra payments. Decide how much extra you can afford to pay each month, and stick to that goal. Even small extra payments can make a big difference over time.

- Use the snowball or avalanche method. These methods can help you stay motivated and organized as you pay off your debt. The snowball method involves paying off the smallest debt first, while the avalanche method involves paying off the debt with the highest interest rate first.

Seek Professional Help

If you’re struggling to manage your debt on your own, don’t hesitate to seek professional help. A credit counselor can provide you with personalized advice and support, and they can also help you negotiate with your creditors.

- Contact a reputable credit counseling agency. There are many credit counseling agencies available, so be sure to do your research and choose one that is reputable and experienced.

- Get a free consultation. Many credit counseling agencies offer free consultations, so take advantage of this opportunity to learn more about their services.

- Be honest and transparent. When you meet with a credit counselor, be honest about your financial situation and your goals. The counselor can help you develop a plan that works for you.

What is the most effective way to manage credit card debt?

The most effective way to manage credit card debt is to develop a comprehensive strategy that combines several approaches. There is no one-size-fits-all solution, and the best approach will vary depending on your individual circumstances and the amount of debt you have. However, some common strategies that can be effective include:

1. Create a Budget

The first step is to understand where your money is going. Creating a budget can help you identify areas where you can cut back on spending, which can free up more money to pay down your debt.

- Track your spending for a month or two to see where your money is going.

- Create a realistic budget that includes all of your essential expenses and your debt payments.

- Stick to your budget as closely as possible.

2. Make More than the Minimum Payment

The minimum payment on a credit card is designed to keep your account in good standing, but it will take you many years to pay off the debt if you only make the minimum payment. The more you can pay each month, the faster you will pay off your debt and the less interest you will accrue.

- Identify any areas where you can cut back on spending to free up more money for debt payments.

- Set up automatic payments to ensure you don’t miss a payment.

- Consider a debt consolidation loan to combine your debt into a single loan with a lower interest rate.

3. Prioritize Your Debt

Not all debt is created equal. Some types of debt, such as credit card debt, have higher interest rates than others. It’s important to prioritize your debt and pay down the debt with the highest interest rate first.

- Identify the debt with the highest interest rate and focus on paying it down first.

- Use the «snowball method» to pay down the debt with the smallest balance first, which can provide a sense of progress and motivation.

- Use the «avalanche method» to pay down the debt with the highest interest rate first, which can save you the most money in the long run.

4. Explore Debt Management Options

There are a number of debt management options available, such as debt consolidation loans, balance transfer credit cards, and debt management programs. These options can help you pay off your debt faster and save money on interest charges.

- Shop around for the best interest rates and terms for a debt consolidation loan.

- Transfer your balances to a balance transfer credit card with a 0% introductory APR to give you time to pay down your debt without accruing interest.

- Consider a debt management program if you are struggling to manage your debt on your own. A debt management program can help you negotiate with your creditors to reduce your monthly payments and interest rates.

5. Avoid Further Debt

Once you have started to make progress on paying down your debt, it’s important to avoid taking on further debt. This means being mindful of your spending habits and resisting the temptation to use credit cards for unnecessary purchases.

- Use cash or a debit card instead of credit cards for everyday purchases.

- Set a spending limit for yourself and stick to it.

- Avoid impulse purchases and only buy things that you can afford to pay for in cash.

How can I legally get rid of my credit card debt?

There are a few legal ways to get rid of your credit card debt. You can pay it off, consolidate it, negotiate a settlement, or file for bankruptcy.

Pay off your credit card debt

The most common and effective way to get rid of your credit card debt is to pay it off. You can do this by making more than the minimum payment each month, or by paying off the entire balance.

Make more than the minimum payment each month. This is the most common way to pay off credit card debt. You can make more than the minimum payment each month by setting a budget and allocating more money to your debt payments.

Pay off the entire balance. This is the fastest way to get rid of your credit card debt. If you have the financial means, you can pay off the entire balance of your credit card.

Consolidate your credit card debt

If you have multiple credit cards with high balances, you can consolidate your debt by taking out a personal loan or a balance transfer credit card. This will allow you to combine your debt into one loan with a lower interest rate.

Take out a personal loan. This is a good option if you have good credit and can get a low interest rate. You can use the money from the loan to pay off your credit card balances.

Balance transfer credit card. This is a good option if you can find a credit card with a 0% introductory APR for a certain period of time. You can transfer your credit card balances to the new card and have time to pay them off at 0% interest.

Negotiate a settlement

You may be able to negotiate a settlement with your credit card issuer. This means that you will pay a lower amount than what you owe in full, but you will still need to pay something. This is a good option if you are unable to pay off your debt in full.

Contact your credit card issuer. You can contact your credit card issuer and ask to negotiate a settlement. Be prepared to provide information about your financial situation.

Consider a debt settlement company. There are companies that specialize in negotiating settlements with creditors. These companies will charge a fee for their services, but they can help you get a lower settlement amount.

File for bankruptcy

If you are unable to pay off your credit card debt through any of the above methods, you may need to file for bankruptcy. This is a legal process that allows you to discharge your debts, but it will have a significant impact on your credit score.

Chapter 7 bankruptcy. This is a type of bankruptcy that allows you to discharge most of your unsecured debts, including credit card debt.

Chapter 13 bankruptcy. This is a type of bankruptcy that allows you to create a payment plan to pay off your debts over time.

Get professional help

If you are struggling with credit card debt, it is important to get professional help. A credit counselor can help you develop a budget, negotiate with your creditors, and find the best solution for your situation.

How to manage debt without sacrificing your financial goals?

Create a Budget and Stick to It

The first step to managing debt without sacrificing your financial goals is to create a budget and stick to it. This means tracking your income and expenses, identifying areas where you can cut back, and setting realistic spending limits. Once you have a budget in place, you can start to develop a plan for paying down your debt.

- Track your income and expenses. Use a budgeting app, spreadsheet, or notebook to track where your money is going each month.

- Identify areas where you can cut back. Look for ways to reduce your spending on non-essential items.

- Set realistic spending limits. Once you know how much you can afford to spend each month, stick to your budget.

Prioritize Your Debt

Once you have a budget in place, you need to prioritize your debt. This means focusing on paying down the debt with the highest interest rate first, as this will save you the most money in the long run. There are a few different methods you can use to prioritize your debt, such as the avalanche method or the snowball method.

- Avalanche Method. This method involves paying down the debt with the highest interest rate first, regardless of the balance.

- Snowball Method. This method involves paying down the debt with the smallest balance first, regardless of the interest rate. This can be a good option if you want to see quick progress and stay motivated.

Negotiate with Creditors

If you are struggling to make your debt payments, you can try negotiating with your creditors. They may be willing to lower your interest rate, reduce your monthly payments, or even forgive some of your debt.

- Contact your creditors. Explain your situation and ask for help.

- Be polite and professional. This will make it more likely that your creditors will be willing to work with you.

- Be prepared to negotiate. You may not get everything you want, but it’s worth trying to negotiate a better deal.

Consider a Debt Consolidation Loan

A debt consolidation loan can be a helpful way to manage debt if you have multiple high-interest loans. This type of loan allows you to combine all of your debt into one loan with a lower interest rate. This can save you money on interest and make it easier to keep track of your payments.

- Shop around for the best rates. Compare interest rates from different lenders before you choose a loan.

- Make sure you can afford the monthly payments. Before you take out a consolidation loan, make sure you can afford the new monthly payments.

- Avoid using credit cards after you consolidate your debt. This will help you avoid accumulating more debt and make it easier to pay off your consolidation loan.

Don’t Give Up on Your Financial Goals

Managing debt can be a long and challenging process, but it’s important to remember that it’s possible to achieve your financial goals even if you have debt. Just stay focused, be patient, and make a plan to pay down your debt as quickly as possible.

- Remember why you set your financial goals. This will help you stay motivated.

- Be patient. It takes time to pay down debt. Don’t get discouraged if you don’t see results right away.

- Celebrate your progress. As you make progress toward your debt goals, celebrate your accomplishments.

Frequently Asked Questions

What is the best way to manage credit card debt without sacrificing my lifestyle?

There is no one-size-fits-all answer to this question, as the best way to manage credit card debt without sacrificing your lifestyle will vary depending on your individual circumstances. However, there are a few general strategies you can consider.

One option is to focus on reducing your spending. This may involve making some tough choices, such as cutting back on non-essential expenses or finding cheaper alternatives to your usual activities. However, it can be an effective way to free up cash flow that you can then use to pay down your debt.

Another option is to increase your income. This could involve getting a second job, taking on freelance work, or starting a side hustle. By increasing your income, you’ll have more money available to put towards your debt payments.

Finally, you may also want to consider negotiating with your creditors. If you are struggling to make your payments, you may be able to negotiate a lower interest rate or a payment plan that is more manageable for you.

What are some tips for reducing my credit card spending?

There are a number of things you can do to reduce your credit card spending. Some simple tips include:

• Track your spending: By tracking your spending, you can get a better understanding of where your money is going and identify areas where you can cut back. You can use a budgeting app, a spreadsheet, or even just a pen and paper to track your spending.

• Set a budget: A budget can help you stay on track with your spending goals and avoid overspending. Make sure to allocate money for essential expenses, such as housing, food, and transportation, and then set aside a portion for discretionary spending.

• Cut back on non-essential expenses: Non-essential expenses are things that you don’t need to live. These might include things like dining out, entertainment, and shopping. By cutting back on these expenses, you can free up cash flow to pay down your debt.

• Find cheaper alternatives: There are often cheaper alternatives to your usual activities. For example, you can watch movies at home instead of going to the cinema, or cook at home instead of eating out.

What are some ways to increase my income?

There are a number of ways to increase your income, such as:

• Get a second job: This can be a great way to earn extra money quickly. You can look for part-time or full-time jobs in your area, or even consider working from home.

• Take on freelance work: If you have skills or experience that you can offer, you can find freelance work online or through local networks. There are many websites and platforms that connect freelancers with clients.

• Start a side hustle: There are many different ways to start a side hustle. You could start a blog, create and sell products online, or offer services such as pet sitting, dog walking, or house cleaning.

• Negotiate a raise at your current job: If you’re a good employee, you may be able to negotiate a raise at your current job. Be prepared to highlight your accomplishments and contributions to the company.

What are some things to consider when negotiating with creditors?

When negotiating with creditors, it’s important to be polite and professional. You should also be prepared to provide information about your financial situation, such as your income and expenses. Here are some things to consider when negotiating with creditors:

• Know your rights: It’s important to understand your rights as a consumer. You should know what you’re entitled to and what your creditors are obligated to do.

• Be prepared to negotiate: You should be prepared to negotiate a lower interest rate, a payment plan, or a combination of both. Be realistic about what you can afford to pay.

• Get everything in writing: Once you’ve reached an agreement with your creditor, make sure to get it in writing. This will help to ensure that both parties are on the same page.