A good credit score is essential for many aspects of your financial life, from securing loans and mortgages to getting lower interest rates and insurance premiums. However, building and maintaining a strong credit score can seem daunting. One of the most important factors influencing your credit score is your payment history. Timely payments account for a significant portion of your overall score, making it a crucial area to focus on. This article will explore how to improve your credit score by establishing a pattern of timely payments, highlighting key strategies and tips to help you navigate this aspect of credit management.

Here’s the HTML code with the H2 and H3 subtitles, detailed explanations, and a table summarizing the information:

The Power of Timely Payments: A Simple Path to a Better Credit Score

Understanding the Impact of Late Payments

Late payments are a significant factor in lowering your credit score. When you don’t pay your bills on time, lenders perceive you as a higher risk, negatively impacting your creditworthiness. This can lead to higher interest rates on loans and difficulty obtaining credit in the future.

Building a Positive Payment History

A consistent track record of making payments on time is crucial for improving your credit score. This demonstrates to lenders that you are a responsible borrower. Even small improvements in payment habits can make a noticeable difference over time.

Set Up Payment Reminders and Autopay

Technology can be your ally in staying on top of your bills. Set up reminders on your calendar or use automated payment systems like autopay. This ensures payments are made automatically on time, eliminating the risk of forgetting or missing a due date.

Communicate with Creditors in Case of Difficulty

If you are facing temporary financial challenges and are unable to make a payment on time, reach out to your creditors. They may be willing to work with you to create a payment plan or offer a temporary hardship program. Proactive communication is key to avoiding further damage to your credit score.

The Importance of Credit Utilization

While timely payments are crucial, it’s also important to keep your credit utilization ratio (the amount of credit you use compared to your total available credit) in check. Aim to keep it below 30%, as higher utilization can negatively impact your score.

| Credit Score Improvement Strategy | Explanation |

|---|---|

| Make Payments on Time | Consistent on-time payments demonstrate financial responsibility and positively impact your credit score. |

| Set Up Payment Reminders | Use technology to remind you of due dates and avoid late payments. |

| Utilize Autopay | Automate your payments to ensure timely payments without manual effort. |

| Communicate with Creditors | Reach out to creditors if you face difficulty making payments on time to explore options like payment plans. |

| Maintain Low Credit Utilization | Keep your credit utilization below 30% by using only a portion of your available credit. |

How can I improve my credit score with late payments?

How to Improve Your Credit Score After Late Payments

Late payments can significantly hurt your credit score. Fortunately, there are several strategies you can employ to repair the damage and improve your credit standing over time.

Pay Your Bills On Time

The most important step to improving your credit score after late payments is to start paying all your bills on time. This means making all payments due within the grace period, even if it’s just a few days late.

- Set up automatic payments for recurring bills. This ensures that you never miss a payment due to forgetfulness or being busy.

- Use a calendar or reminder app to track upcoming due dates.

- Pay your bills as soon as you receive them, not just when they’re due.

Get a Secured Credit Card

If you have a history of late payments, it can be difficult to get approved for a traditional credit card. A secured credit card requires you to make a deposit that serves as your credit limit. This helps lenders feel more secure about lending you money, and it gives you a chance to build positive credit history.

- Choose a secured credit card with a low annual fee.

- Use the card regularly for small purchases and pay it off in full each month.

- After a few months of responsible use, ask the issuer to graduate the card to an unsecured card.

Dispute Errors on Your Credit Report

Late payments might be the result of errors on your credit report. You can dispute these errors with the credit bureaus to correct your credit history.

- Review your credit reports from all three bureaus: Equifax, Experian, and TransUnion.

- If you find any inaccurate information, file a dispute with the credit bureau.

- Provide documentation to support your claims.

Consider a Credit Counseling Agency

A credit counseling agency can help you create a budget and develop a plan to manage your debt effectively. They can also negotiate with your creditors on your behalf to lower interest rates or reduce your monthly payments.

- Choose a reputable and accredited counseling agency.

- Be transparent about your financial situation with the counselor.

- Follow their advice and be committed to making your payments on time.

How many months of on time payments to improve credit score?

How long does it take to improve a credit score with on-time payments?

There is no magic number of months to see a significant improvement in your credit score from making on-time payments. The impact depends on several factors, including your starting credit score, the length of your credit history, and other factors like credit utilization, recent inquiries, and negative marks on your credit report. However, consistently making on-time payments demonstrates responsible financial behavior and can contribute to a gradual improvement in your score over time.

How do on-time payments affect my credit score?

On-time payments are a crucial factor in calculating your credit score. Credit scoring models like FICO assign a significant weight to payment history, typically around 35% of your overall score. Making timely payments shows lenders that you are reliable and capable of managing debt, leading to a positive impact on your credit score.

What other factors affect credit score improvement?

While on-time payments are crucial, they are not the only factor influencing your credit score. Other factors include:

- Credit utilization: This refers to the amount of credit you are using compared to your total available credit. Aim to keep your credit utilization below 30% for optimal credit score benefits.

- Credit mix: Having a mix of different credit accounts, such as credit cards, installment loans, and mortgages, can indicate responsible credit management and potentially boost your score.

- Length of credit history: The longer your credit history, the better your score generally tends to be. Avoid closing old accounts, as this can negatively impact your average account age.

- New credit inquiries: Every time you apply for credit, a hard inquiry is placed on your credit report. Too many hard inquiries can negatively impact your score, so limit your applications to only those you truly need.

- Negative marks: Late payments, collections, charge-offs, and bankruptcies can significantly hurt your score. If you have any negative marks, work on resolving them and building a positive payment history to offset their impact.

What is the minimum time required for on-time payments to show?

While there is no minimum time for on-time payments to show, you can generally start seeing a positive change in your credit score within a few months of consistently making timely payments. However, the improvement may be gradual, and significant changes could take several months or even longer.

How to monitor credit score improvement

To track your progress, it is recommended to regularly check your credit report and score from all three major credit bureaus, Equifax, Experian, and TransUnion. You can access free credit reports from AnnualCreditReport.com. Additionally, you can utilize credit monitoring services that provide regular updates on your score and alert you to any significant changes.

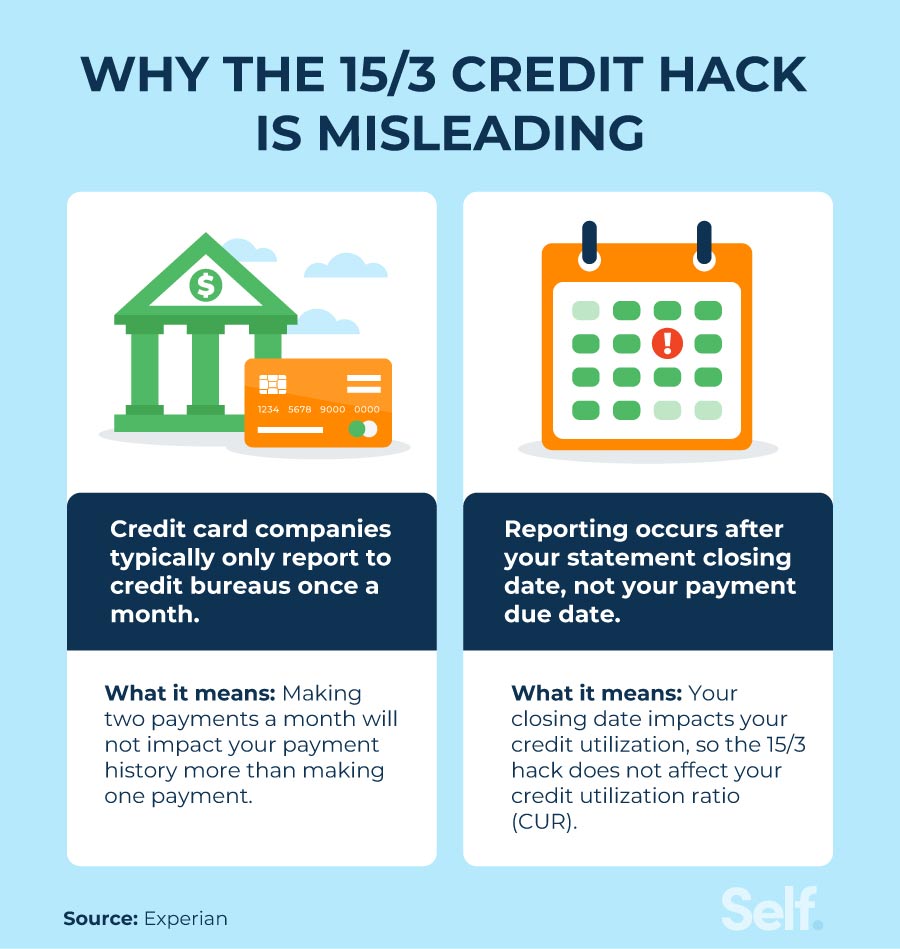

What is the 15-3 payment trick?

The 15-3 payment trick is a budgeting method that aims to pay off debt faster and build wealth. It encourages you to allocate 15% of your income to debt repayment and 3% to savings or investments.

How does the 15-3 payment trick work?

This method breaks down your income into three categories:

- Essential Expenses (50%): Rent, utilities, groceries, transportation, etc.

- Debt Payments (15%): Focus on high-interest debt first.

- Savings and Investments (3%): Building an emergency fund, investing in retirement, etc.

What are the benefits of the 15-3 payment trick?

- Faster Debt Repayment: Prioritizing debt repayment helps you get out of debt sooner and save on interest.

- Building Financial Security: Regular savings and investments build a financial cushion for unexpected expenses and future goals.

- Improved Financial Discipline: The method encourages you to track your spending and make conscious financial decisions.

What are the potential drawbacks of the 15-3 payment trick?

- May be restrictive: The fixed percentages might not suit everyone’s financial situation, especially those with high essential expenses.

- Doesn’t account for all financial goals: It doesn’t allocate for non-essential expenses or specific goals like homeownership or education.

- May be too conservative: Some people might find the savings percentage too low and prefer to allocate more to investments.

How to adjust the 15-3 payment trick to your situation?

- Consider your income and expenses: Adjust the percentages based on your financial situation and goals.

- Prioritize your needs: Allocate more to essential expenses if necessary and less to savings if you’re in debt.

- Regularly review your budget: Make adjustments as your income and expenses change.

How to get 800 credit score in 45 days?

It is impossible to guarantee a credit score of 800 in 45 days. Credit scores are based on a variety of factors, including payment history, credit utilization, length of credit history, credit mix, and new credit. These factors take time to improve, and it is unlikely that significant progress can be made in such a short time frame.

However, here are some tips that may help you improve your credit score over time:

Pay Your Bills On Time

- Set reminders for all your bill due dates.

- Enroll in automatic payments for all of your recurring bills.

- Create a budget and prioritize your bills to ensure you are paying them on time.

Lower Your Credit Utilization Rate

- Pay down any outstanding balances on your credit cards and other revolving accounts.

- Avoid opening new accounts that will increase your overall credit utilization rate.

- Keep your credit card balances below 30% of your credit limit.

Don’t Apply for New Credit

- Avoid applying for new credit cards or loans, as this can lower your credit score.

- Only apply for credit if you truly need it and have already done your research.

Become an Authorized User

- Ask a family member or friend with good credit to add you as an authorized user on their account.

- This can help to boost your credit score by adding a positive credit history to your report.

- Be careful to choose an account with a responsible user who will not negatively impact your credit score.

Monitor Your Credit Report Regularly

- Check your credit report for errors and inaccuracies that could be affecting your score.

- Use a credit monitoring service to track your credit score and receive alerts about changes to your report.

Frequently Asked Questions

How does paying bills on time improve my credit score?

On-time payments are a significant factor in determining your credit score. They account for a large portion of your credit score calculation, typically around 35%. When you consistently make payments by the due date, it shows lenders that you are a responsible borrower and can be trusted to repay your debts. This positive track record makes you a more attractive borrower in the future, leading to better interest rates and loan terms.

What happens if I make a late payment?

Making a late payment can have a negative impact on your credit score. A late payment is typically reported to credit bureaus within 30 days of the missed payment. This can lower your credit score and potentially increase your interest rates on future loans. The severity of the impact depends on factors such as the amount of the late payment, the frequency of late payments, and your overall credit history.

How often should I check my credit score?

It’s recommended to check your credit score at least once a year, ideally every three to six months. This allows you to track your progress and identify any potential issues. You can access your credit score through credit reporting agencies such as Equifax, Experian, and TransUnion. Checking your credit score regularly can help you catch any errors and take steps to improve your credit history.

What are some tips for making timely payments?

Here are some tips for making timely payments:

- Set up automatic payments: This ensures that your bills are paid on time, even if you forget.

- Use calendar reminders: Mark important due dates on your calendar or use a reminder app.

- Consider a budgeting app: These apps can help you track your spending and ensure you have enough funds to cover your bills.

- Pay bills early: If possible, pay your bills a few days before the due date to avoid any potential late fees or reporting delays.