Managing your money can feel overwhelming, especially if you’re struggling to make ends meet. But fear not! Creating a budget doesn’t have to be a chore. In fact, it can be a powerful tool to achieve your financial goals, whether it’s saving for a down payment on a house, paying off debt, or simply having more financial peace of mind. This article will guide you through the steps of creating a budget that actually works for you, taking into account your individual needs and spending habits. We’ll explore different budgeting methods, tips for tracking your expenses, and strategies for sticking to your plan. Get ready to take control of your finances and achieve financial freedom!

Crafting a Budget That Works for You

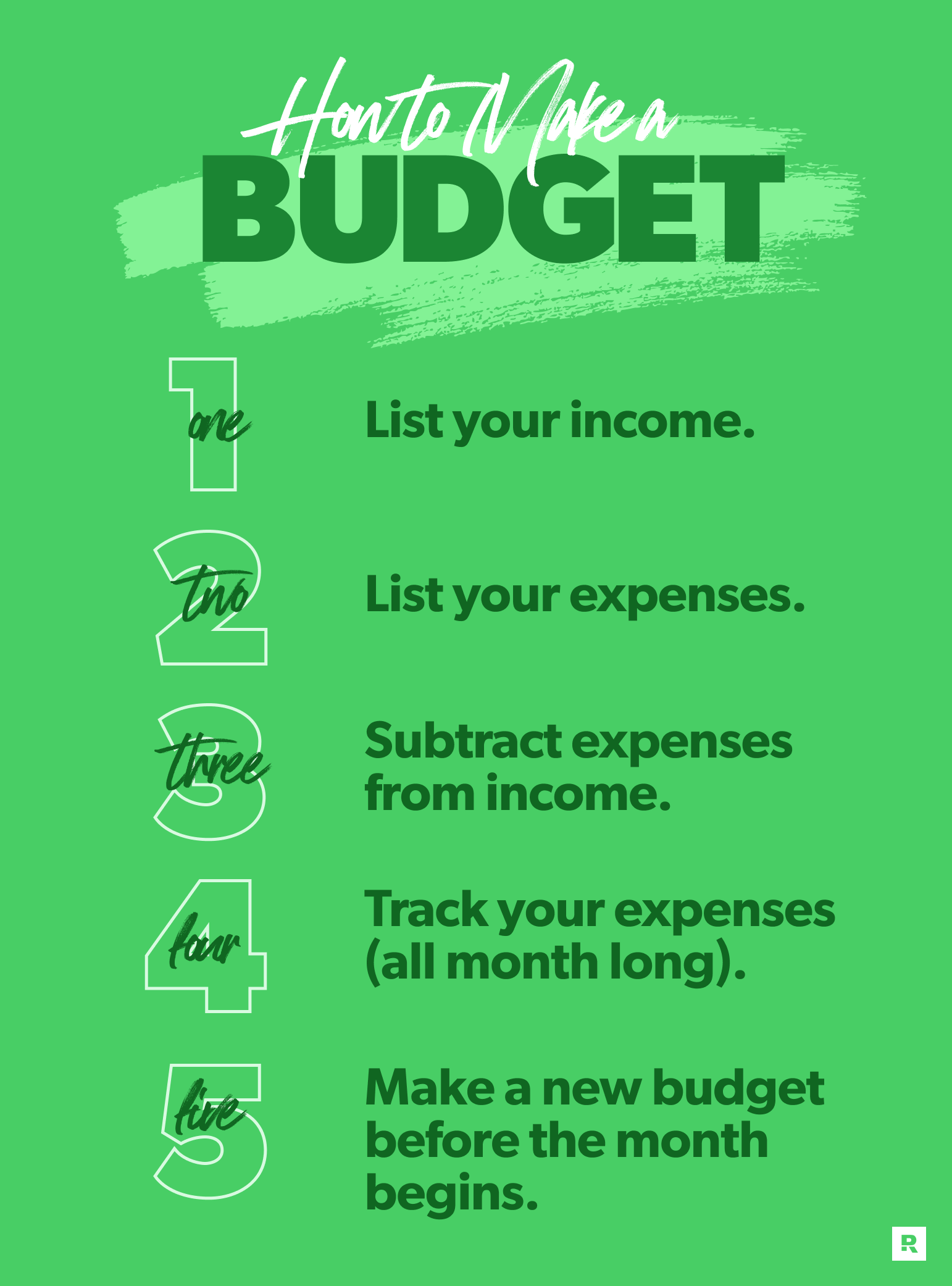

1. Track Your Spending

The first step to creating a budget that works is understanding where your money is going. This can be done by tracking your spending for a month or two. There are many ways to track your spending, such as using a spreadsheet, a budgeting app, or even just keeping a notebook. Once you know where your money is going, you can start to make changes to your spending habits.

2. Set Financial Goals

What are your financial goals? Do you want to save for a down payment on a house, pay off debt, or retire early? Once you know what your goals are, you can start to create a budget that will help you achieve them. It’s important to be realistic about your goals and to set a timeline for achieving them. This will help you stay motivated and on track.

3. Create a Budget

Once you know where your money is going and what your financial goals are, you can start to create a budget. There are many different budgeting methods, but the most important thing is to find one that works for you. One common method is the 50/30/20 rule. This rule suggests allocating 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. You can adjust these percentages to fit your own needs and goals.

4. Stick to Your Budget

The hardest part of budgeting is sticking to it. This requires discipline and self-control. However, there are a few things you can do to make it easier. One is to set up automatic transfers from your checking account to your savings account. This will help you save money without even thinking about it. Another is to find ways to cut back on your spending. This may mean eating out less, buying generic brands, or finding free or low-cost entertainment options.

5. Review and Adjust Your Budget

It is important to review and adjust your budget regularly. This will help you stay on track with your financial goals and make sure that your budget is still working for you. Life changes, and your budget should change with it. As your income increases, so should your savings. As you pay off debt, you may want to re-allocate that money to other goals. Reviewing your budget regularly will help you stay on top of your finances and ensure you are on the right track to reach your financial goals.

How to make a budget that actually works for you?

Track Your Spending

Knowing where your money is going is the first step to budgeting effectively. There are many ways to track your spending. You can use a spreadsheet, a budgeting app, or even just a notebook. The important thing is to be consistent and to record all of your expenses, no matter how small. This allows you to identify areas where you can save.

- Use a budgeting app: These apps make tracking your spending easy. They often have features that help you categorize your spending and set budgets for different categories.

- Keep a spreadsheet: This is a more manual approach, but it can be just as effective. You can create a spreadsheet to track your income and expenses, and then use it to create a budget.

- Use a notebook: If you prefer a more analog approach, you can keep a notebook to track your spending. Just make sure to be consistent and to record all of your expenses.

Set Realistic Goals

When setting financial goals, it’s important to be realistic. Don’t set yourself up for failure by setting unrealistic expectations. For example, if you’re trying to save for a down payment on a house, it’s unrealistic to expect to save thousands of dollars each month. Instead, start small and gradually increase your savings as your income grows.

- Start small: It’s better to set small, achievable goals and gradually work your way up to larger goals.

- Be specific: Set specific goals rather than vague ones. For example, instead of saying “I want to save money,” say “I want to save $1,000 by the end of the year.”

- Set a timeline: This will help you stay on track and motivated. For example, you could set a goal to save $100 per month for the next year.

Create a Budget

Once you know where your money is going, you can create a budget. This is a plan for how you will spend your money each month. It should include your income, your fixed expenses (such as rent or mortgage payments), and your variable expenses (such as groceries, entertainment, and clothing).

- Use the 50/30/20 rule: This rule suggests that you allocate 50% of your income to needs (housing, food, transportation), 30% to wants (entertainment, dining out, hobbies), and 20% to savings and debt repayment.

- Use a zero-based budget: This budgeting method assigns every dollar of your income to a specific category. This can help you avoid overspending.

- Use a budgeting app: There are many budgeting apps available that can help you create and track your budget.

Review and Adjust

A budget isn’t a set-it-and-forget-it plan. You should review and adjust your budget regularly to make sure it’s still working for you. As your income changes or your spending habits change, you may need to make adjustments to your budget.

- Review your budget monthly: This will allow you to see if you’re staying on track and to make any necessary adjustments.

- Be flexible: Life happens, and your budget may need to be adjusted from time to time. Don’t be afraid to make changes as needed.

- Don’t be afraid to experiment: If your budget isn’t working for you, try different methods until you find one that does.

Automate Your Savings

One of the best ways to make sure you’re saving money is to automate your savings. This means setting up automatic transfers from your checking account to your savings account. This way, you don’t have to think about it, and you’ll be saving money without even realizing it.

- Set up automatic transfers: Most banks allow you to set up automatic transfers from your checking account to your savings account. This can be a great way to save money without having to think about it.

- Use a savings app: There are many savings apps available that can help you automate your savings. These apps often have features that make it easy to set savings goals and track your progress.

- Consider a high-yield savings account: These accounts offer higher interest rates than traditional savings accounts, so you can earn more money on your savings.

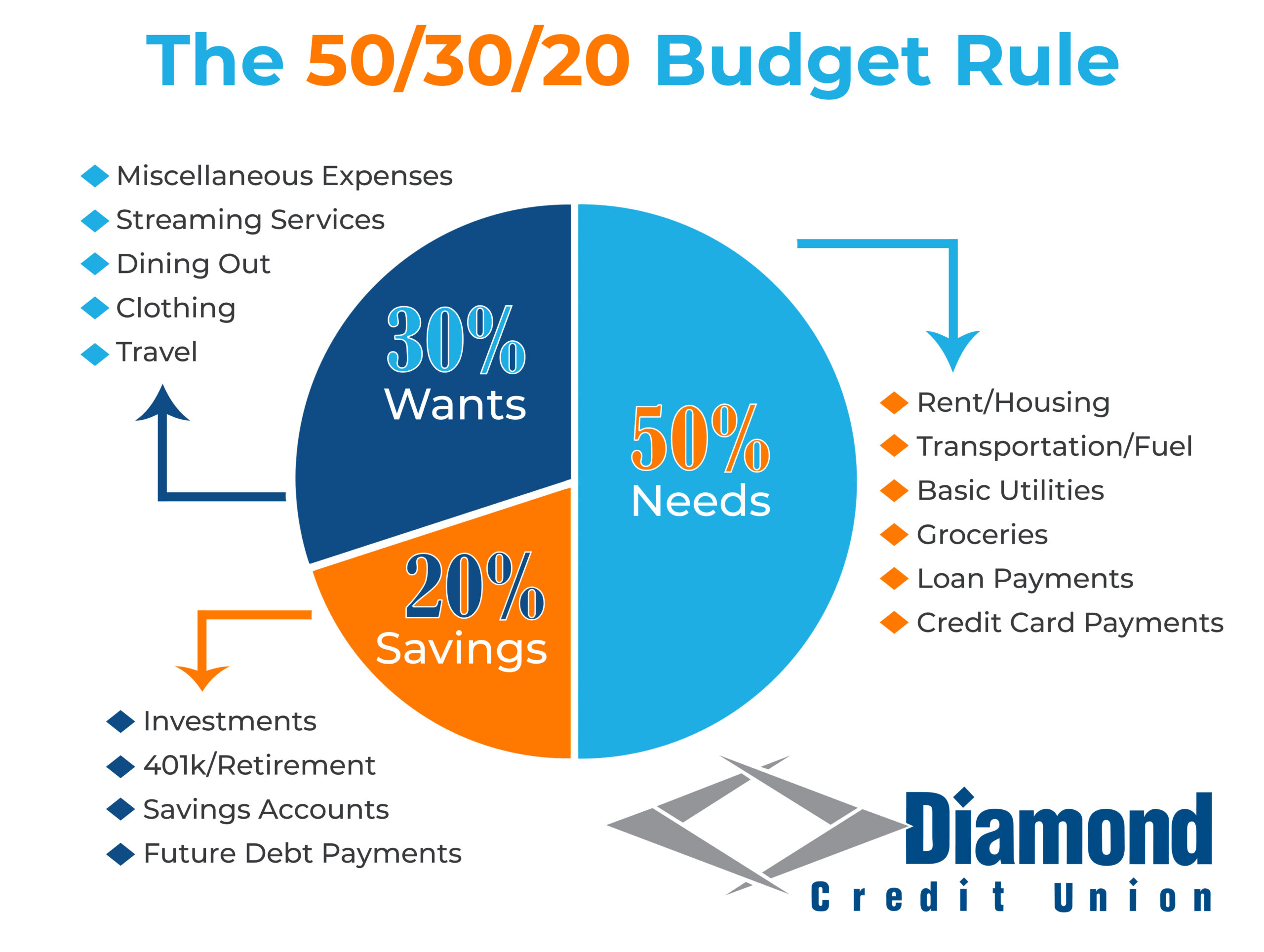

What is the 50/30/20 budget rule?

What is the 50/30/20 Budget Rule?

The 50/30/20 budget rule is a simple budgeting method that divides your after-tax income into three categories: needs, wants, and savings. The rule suggests allocating:

50% of your income to needs: These are essential expenses like housing, food, utilities, transportation, and healthcare.

30% of your income to wants: These are discretionary expenses like dining out, entertainment, vacations, and hobbies.

20% of your income to savings and debt repayment: This includes contributions to retirement accounts, emergency funds, and paying off loans.

Benefits of the 50/30/20 Budget Rule

The 50/30/20 budget rule offers several benefits, including:

- Simplicity: The rule is straightforward and easy to understand, making it accessible for individuals of all financial backgrounds.

- Financial Control: By allocating income systematically, you gain a clear picture of your spending and can identify areas for potential savings.

- Prioritizing Needs: Ensuring that your needs are covered first helps maintain financial stability and avoid debt.

- Building Savings: Dedicating a significant portion of your income to savings helps achieve your financial goals, such as retirement planning or purchasing a home.

How to Implement the 50/30/20 Budget Rule

Implementing the 50/30/20 budget rule involves a few steps:

- Track your spending: Monitor your income and expenses for a month to understand your current spending patterns.

- Calculate your net income: Subtract taxes and other deductions from your gross income to determine your after-tax income.

- Allocate your income: Divide your net income into the three categories (50% needs, 30% wants, 20% savings).

- Adjust as needed: Regularly review your budget and make adjustments based on changes in your income or expenses.

Flexibility of the 50/30/20 Budget Rule

The 50/30/20 budget rule is a guideline, and its specific percentages can be adjusted to suit individual needs and circumstances.

- Higher Needs Percentage: If your living costs are high, you might need to allocate more than 50% to needs.

- Lower Wants Percentage: If you prioritize saving and debt repayment, you could reduce the wants category to 20% or less.

Limitations of the 50/30/20 Budget Rule

While the 50/30/20 budget rule is a helpful starting point, it may not be suitable for everyone.

- Not a One-Size-Fits-All Solution: The rule doesn’t account for individual financial situations, goals, and risk tolerance.

- Oversimplification: It might not address all financial needs, such as unexpected expenses or specific financial goals.

- Requires Discipline: Following the rule requires commitment and discipline to stick to the allocated percentages.

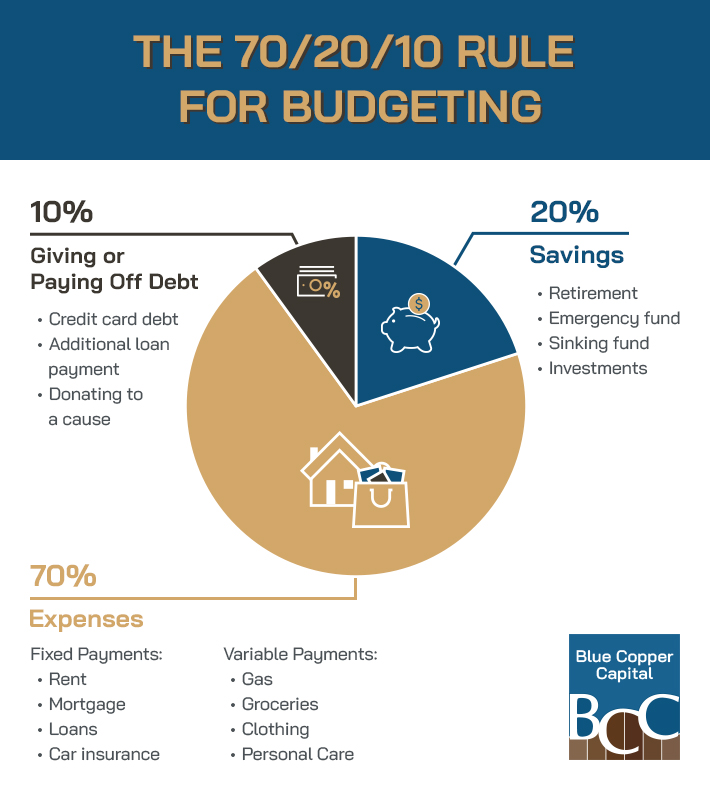

What is the 70/20/10 rule money?

What is the 70/20/10 Rule?

The 70/20/10 rule is a simple budgeting strategy that suggests dividing your after-tax income into three categories: 70% for needs, 20% for wants, and 10% for savings and debt repayment.

Needs

Needs are essential expenses that are required for survival and well-being. This includes:

- Housing: Rent or mortgage payments.

- Food: Groceries and dining out.

- Utilities: Electricity, gas, water, internet, and phone.

- Transportation: Car payments, gas, and public transportation.

- Healthcare: Insurance premiums and medical expenses.

- Insurance: Home, auto, and health insurance.

Wants

Wants are non-essential expenses that provide pleasure or convenience but are not necessary for survival. This includes:

- Entertainment: Movies, concerts, and sporting events.

- Dining out: Restaurants and cafes.

- Travel: Vacations and weekend getaways.

- Shopping: Clothing, accessories, and electronics.

- Hobbies: Sports, music, and art supplies.

Savings

Savings are the portion of your income that you set aside for future financial goals. This includes:

- Emergency fund: A cushion to cover unexpected expenses.

- Retirement savings: Contributions to 401(k)s, IRAs, and other retirement accounts.

- Down payment: Savings for a house, car, or other major purchase.

- Investment goals: Funds for stocks, bonds, and other investments.

Debt Repayment

Debt repayment is the portion of your income that you allocate to paying off existing debt. This includes:

- Credit card debt: Paying down the balance on your credit cards.

- Student loan debt: Making payments on your student loans.

- Personal loans: Repaying any other personal loans you have.

How do you come up with a realistic budget?

Track Your Spending

Before you can create a budget, you need to know where your money is going. For a month or two, track every dollar you spend. This can be done with a notebook, spreadsheet, or budgeting app. Be sure to track both your fixed expenses (rent, utilities, etc.) and your variable expenses (groceries, entertainment, etc.).

- Use a budgeting app or spreadsheet to keep track of your spending.

- Keep receipts for all purchases to make tracking easier.

- Categorize your spending so you can see where your money is going.

Determine Your Income

Once you know where your money is going, you need to know how much money you have coming in. This includes your salary, any other income sources (such as investments or part-time jobs), and any regular payments you receive (such as child support or alimony).

- List all sources of income.

- Calculate your net income (income after taxes and deductions).

- Consider any irregular income sources.

Create a Budget Plan

Now it’s time to create a budget plan that outlines how you will spend your money. This is where you allocate your income to different categories, such as housing, food, transportation, entertainment, and savings. Be sure to be realistic with your spending and make sure that your expenses are less than or equal to your income.

- Prioritize your needs.

- Allocate your income to different categories.

- Leave room for unexpected expenses.

Stick to Your Budget

Once you have a budget in place, it’s important to stick to it. This can be challenging, but it’s essential for reaching your financial goals. There are a few things you can do to make it easier, such as automating your savings and setting up a budget tracker. You can also consider cutting back on unnecessary spending and looking for ways to save money.

- Use a budgeting app or spreadsheet to track your spending.

- Set realistic goals and adjust your budget accordingly.

- Don’t be afraid to make changes to your budget.

Review and Adjust

Your budget isn’t set in stone. You should review and adjust your budget regularly, especially when your income or expenses change. You may also need to make adjustments if you reach a new financial goal or experience a life change.

- Review your budget every month.

- Make adjustments to your budget as needed.

- Don’t be afraid to start over if necessary.

Frequently Asked Questions

What is a budget?

A budget is a plan for how you will spend your money. It tracks your income and expenses so you can see where your money is going and make informed financial decisions. A budget can help you achieve your financial goals, such as saving for a down payment on a house, paying off debt, or investing for retirement.

Why should I create a budget?

Creating a budget can help you manage your money more effectively and achieve your financial goals. It can help you identify areas where you can cut back on spending, track your progress towards your goals, and avoid overspending. A budget can also provide you with peace of mind knowing that you have a plan in place for managing your finances.

How do I create a budget?

To create a budget, you need to track your income and expenses for a period of time, such as a month. You can use a budgeting app, spreadsheet, or notebook to track your spending. Once you have a good understanding of your income and expenses, you can create a budget that allocates your money to different categories, such as housing, food, transportation, and entertainment. You should also consider your financial goals when creating your budget and make sure that you are allocating enough money to reach them.

What are some tips for sticking to my budget?

Sticking to your budget can be challenging, but it’s important to stay consistent. Here are some tips for sticking to your budget:

Track your spending: Monitor your spending regularly to ensure that you are staying within your budget.

Set realistic goals: Make sure your budget goals are achievable, and don’t try to cut back on spending too drastically all at once.

Automate your savings: Set up automatic transfers from your checking account to your savings account so that you can save money consistently.

Find ways to reduce your spending: Look for ways to cut back on your expenses, such as cooking at home more often, finding cheaper alternatives for entertainment, or negotiating bills.

Reward yourself for sticking to your budget: Give yourself a small reward for sticking to your budget, such as a night out with friends or a new book.

Don’t give up: It takes time and effort to stick to a budget, so don’t get discouraged if you slip up occasionally. Just get back on track and keep working towards your financial goals.