Sure, here is an introduction for an article about «How to Build a Financial Legacy with Savings»:

***

The desire to leave behind a legacy is deeply ingrained in human nature. We all want to ensure that our hard work and financial contributions have a lasting impact on our loved ones, our communities, and even the world at large. While many associate legacy building with philanthropy or monumental acts of generosity, a strong financial foundation is the cornerstone of any lasting legacy. This article explores the powerful role of savings in building a financial legacy that transcends generations and empowers your loved ones to achieve their own goals. We will delve into practical strategies for saving effectively, investing wisely, and ensuring your legacy thrives long after you are gone.

***

Building a Strong Financial Legacy Through Savings

Start Saving Early and Often

Saving early and often is crucial for building a financial legacy. It allows your money to compound over time, which means that your earnings grow exponentially as you invest and reinvest.

| Benefits of Early Saving | Explanation |

|---|---|

| Compounding Interest | Earnings on your savings are reinvested, generating more earnings over time. |

| Time Value of Money | Money saved early is worth more in the future due to inflation and potential returns. |

| Financial Stability | Regular saving provides a safety net for unexpected expenses and emergencies. |

Determine Your Financial Goals

Identifying your financial goals is essential for creating a tailored savings plan. What do you envision for your financial future? Do you want to retire comfortably, fund your children’s education, or purchase a dream home?

| Goal Setting | Explanation |

|---|---|

| Retirement Planning | Saving for a comfortable retirement allows you to maintain your lifestyle after leaving the workforce. |

| Education Funding | Saving for college or university expenses ensures your children have access to quality education. |

| Homeownership | Saving for a down payment on a house can make homeownership a reality. |

| Emergency Fund | Having a financial cushion protects you against unexpected expenses or job loss. |

Choose the Right Savings Vehicles

Different saving vehicles cater to different needs and risk tolerances. It’s essential to select vehicles that align with your financial goals and time horizons.

| Savings Vehicles | Explanation |

|---|---|

| High-Yield Savings Accounts | Offer higher interest rates than traditional savings accounts, suitable for short-term savings. |

| Certificates of Deposit (CDs) | Fixed-term investments with guaranteed interest rates, suitable for longer-term savings. |

| Retirement Accounts (401(k), IRA) | Tax-advantaged accounts for saving for retirement, offering potential tax benefits. |

| Investment Accounts | Allow for investing in stocks, bonds, and other assets, offering potential for higher returns. |

Automate Your Savings

Setting up automated savings transfers ensures you consistently save without actively remembering. This removes the burden of manual saving and promotes disciplined saving habits.

| Automation Benefits | Explanation |

|---|---|

| Consistency | Regular transfers ensure consistent saving even when busy or forgetful. |

| Discipline | Automated savings encourage disciplined financial behavior. |

| Time Efficiency | Saving becomes effortless and frees up your time for other activities. |

Review and Adjust Your Plan

Regularly reviewing your savings plan and making adjustments is crucial for staying on track. Life circumstances change, so adapt your strategy to reflect your evolving needs and goals.

| Reviewing and Adjusting | Explanation |

|---|---|

| Assess Progress | Monitor your savings progress and determine if you’re on track to achieve your goals. |

| Evaluate Goals | Revisit your financial goals and make any necessary adjustments based on life changes. |

| Market Conditions | Consider changes in market conditions and make adjustments to your investment strategy. |

| Personal Circumstances | Adjust your savings plan based on changes in income, expenses, or family size. |

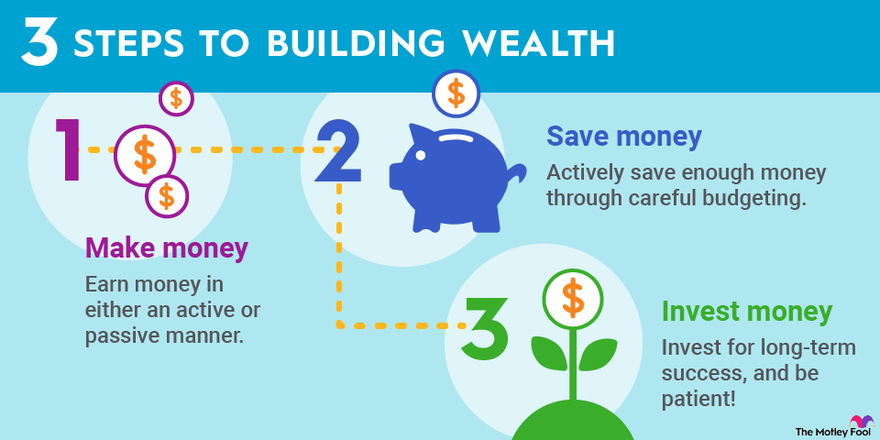

How do you build wealth with savings?

Understanding Compound Interest

Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it. This quote by Albert Einstein highlights the power of compounding, a key concept in wealth building. Essentially, compound interest means earning interest on your initial investment, as well as on the accumulated interest. This snowball effect allows your money to grow exponentially over time. The longer your money stays invested, the more it compounds, leading to significant wealth accumulation.

Setting Financial Goals

Before you start saving, it’s crucial to have a clear picture of your financial goals. What do you want to achieve with your savings? Are you aiming for a comfortable retirement, buying a home, funding your children’s education, or simply building a safety net? Defining your goals will help you determine the amount you need to save and the time frame for achieving them. It’s also essential to set realistic and achievable goals, breaking them down into smaller milestones to maintain motivation and track progress.

Creating a Budget and Sticking to It

A budget is a roadmap to your financial well-being. It outlines how much money you have coming in and how much you’re spending. Creating a budget allows you to identify areas where you can cut back and allocate more towards saving. The key is to track your expenses regularly and make adjustments as needed. It’s also helpful to automate your savings by setting up regular transfers from your checking account to your savings account.

Choosing the Right Savings Vehicles

Not all savings accounts are created equal. Some offer higher interest rates, while others come with specific features or restrictions. It’s essential to research and choose savings vehicles that align with your financial goals and risk tolerance. Consider options like:

- High-yield savings accounts: These offer higher interest rates compared to traditional savings accounts, allowing your money to grow faster.

- Certificates of deposit (CDs): CDs provide a fixed interest rate for a set period, offering a predictable return on your investment. However, you’ll need to commit your money for a specific duration.

- Money market accounts (MMAs): MMAs offer variable interest rates, typically higher than savings accounts but lower than CDs. They also provide limited check-writing privileges.

- Retirement accounts: These accounts, such as 401(k)s and IRAs, offer tax advantages for retirement savings. They allow you to save for retirement and potentially grow your wealth significantly.

Investing for Growth

While savings are essential, investing can be crucial for long-term wealth building. Investing allows your money to potentially grow at a faster rate than savings accounts alone. However, it also involves risk. It’s vital to understand the risks involved, diversify your investments, and seek advice from a qualified financial advisor. Consider options like:

- Stocks: Stocks represent ownership in publicly traded companies. They offer potential for high returns but also come with higher risk.

- Bonds: Bonds are loans to governments or companies. They typically offer lower returns than stocks but are generally considered less risky.

- Mutual funds: Mutual funds pool money from multiple investors to buy a diversified portfolio of assets, offering lower risk and potentially higher returns than investing in individual securities.

- Real estate: Investing in real estate can offer both income and appreciation potential, but it requires significant capital and comes with its own set of risks.

How to build a financial legacy?

Set Clear Financial Goals

Before you can build a financial legacy, you need to have a clear idea of what you want to achieve. What kind of financial future do you envision for yourself and your loved ones? Do you want to leave behind a substantial inheritance, secure their financial independence, or ensure they can pursue their dreams? Define your goals, quantify them with specific numbers, and set realistic timelines for achieving them. This clarity will guide your financial decisions and keep you motivated.

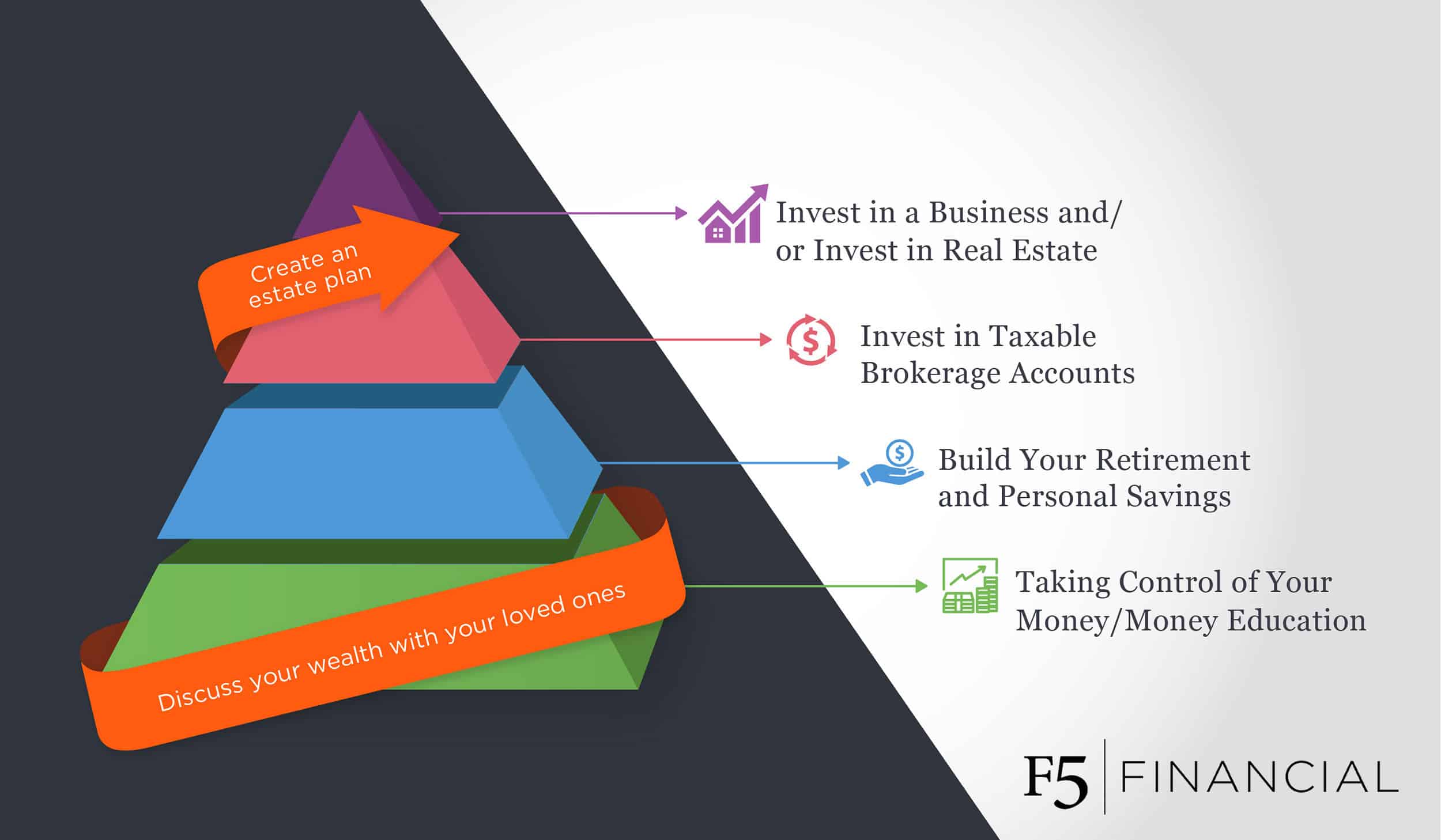

Develop a Solid Financial Plan

A financial plan is the roadmap to building a legacy. It encompasses budgeting, saving, investing, and managing debt. This plan should be tailored to your specific goals, risk tolerance, and time horizon. A financial advisor can help you create a comprehensive plan that includes:

- Budgeting: Track your income and expenses to identify areas for improvement and maximize savings.

- Saving: Establish an emergency fund, contribute to retirement accounts (e.g., 401(k), IRA), and explore other savings vehicles.

- Investing: Diversify your investments across different asset classes (stocks, bonds, real estate) to manage risk and maximize potential returns.

- Managing Debt: Pay down high-interest debt, such as credit card debt, to free up cash flow for other financial goals.

Build a Strong Foundation

A solid financial foundation is essential for building a legacy. This involves:

- Protecting your assets: Purchase insurance policies (life, health, disability) to safeguard your finances against unforeseen events.

- Building good credit: A good credit score unlocks better loan terms, lower interest rates, and greater financial opportunities.

- Managing your risk: Diversify your investments, avoid unnecessary debt, and plan for unexpected expenses to mitigate financial risks.

Invest for the Long Term

Building a financial legacy takes time and patience. Avoid short-term speculation and focus on long-term investing strategies. Consider:

- Investing in the stock market: Through index funds or mutual funds, you can gain exposure to a wide range of companies and industries.

- Investing in real estate: Owning rental properties or investing in REITs can generate passive income and appreciate in value over time.

- Investing in your own business: Starting and growing your own business can create significant wealth and provide a legacy for your family.

Share your Financial Knowledge

Passing on financial knowledge to your loved ones is a crucial part of building a legacy. This could involve:

- Open communication: Discuss your financial goals, plans, and strategies openly with your family members.

- Financial education: Educate them about budgeting, saving, investing, and other essential financial skills.

- Mentorship: Provide guidance and support as they navigate their own financial journeys.

What is the fastest way to create generational wealth?

Investing in Real Estate

Real estate has historically been a strong investment for creating generational wealth. Investing in rental properties can provide a steady stream of passive income that can be passed down to future generations. Real estate values tend to appreciate over time, making it a valuable asset that can be used to build wealth for years to come.

- Buy and hold strategy: Purchasing properties with the intention of holding them for the long term, aiming to benefit from appreciation and rental income.

- Diversification: Investing in a variety of properties in different locations and asset classes to mitigate risk.

- Property management: Hiring professional property managers to handle day-to-day operations and minimize headaches.

Starting a Business

Entrepreneurship can be a powerful engine for generating wealth, particularly when building a successful business that can be passed down to future generations. This can involve creating a scalable company that provides products or services that are in demand.

- Scalability: Building a business with the potential to grow and expand its reach over time.

- Strong brand and reputation: Developing a recognizable brand and a positive reputation in the market.

- Succession planning: Establishing a clear plan for transferring ownership and management of the business to future generations.

Investing in the Stock Market

Investing in the stock market, particularly through index funds and ETFs, can be a reliable way to grow wealth over the long term. This involves diversifying investments across different asset classes and sectors to mitigate risk.

- Long-term investing: Adopting a buy-and-hold approach, allowing investments to grow over time through compounding returns.

- Dollar-cost averaging: Investing a fixed amount at regular intervals, regardless of market fluctuations, to reduce the impact of volatility.

- Diversification: Spreading investments across different sectors, industries, and asset classes to reduce risk.

Investing in Education and Skills

Investing in education and skills development is a powerful way to build human capital, which can lead to higher earning potential and wealth creation. This can involve pursuing higher education, acquiring specialized skills, and continuously learning and adapting.

- Higher education: Pursuing a college degree or professional certification to enhance career prospects.

- Professional development: Investing in training, workshops, and online courses to acquire new skills and stay competitive.

- Mentorship and networking: Seeking guidance from experienced professionals and building relationships to expand knowledge and opportunities.

Saving and Budgeting

Building generational wealth requires a disciplined approach to saving and budgeting. This involves prioritizing saving, controlling expenses, and developing a financial plan that supports long-term goals.

- Emergency fund: Establishing a savings cushion to cover unexpected expenses and prevent financial instability.

- Budgeting: Tracking income and expenses to identify areas for savings and make informed financial decisions.

- Retirement planning: Contributing to retirement accounts to ensure financial security in later years.

How to build generational wealth in 6 steps?

1. Define Your Financial Goals

Before you start building generational wealth, you need to have a clear understanding of what that means for you and your family. What are your financial goals? How much money do you want to accumulate? What do you want to do with that wealth? Once you have a clear understanding of your goals, you can start to develop a plan to achieve them.

- Determine your long-term financial objectives. What do you envision for your family’s future? Do you want to provide financial security for future generations, fund education, or create a legacy?

- Set specific, measurable, achievable, relevant, and time-bound (SMART) goals. This will give you a clear roadmap to track your progress.

- Consider the time horizon for achieving your goals. Generational wealth is built over decades, so it’s important to factor in a long-term perspective.

2. Create a Budget and Track Your Spending

A budget is essential for building generational wealth. It helps you to see where your money is going and identify areas where you can save. Once you have a budget, it’s important to track your spending to make sure you’re sticking to it. There are many budgeting apps and tools available to help you.

- Identify your income and expenses. Categorize your expenses and determine which are essential and which can be reduced.

- Set a realistic budget that allows for savings and investments. Allocate a portion of your income to savings and investments, even if it’s a small amount at first.

- Track your spending regularly to ensure you’re staying within your budget. Use budgeting apps, spreadsheets, or other methods to monitor your finances.

3. Save and Invest Regularly

Saving and investing are essential for building generational wealth. The sooner you start, the more time your money has to grow. There are many different savings and investment options available, so it’s important to choose the ones that are right for you.

- Establish an emergency fund. This will provide a financial safety net in case of unexpected expenses.

- Start investing early and consistently. Even small contributions can add up over time, thanks to compounding interest.

- Diversify your investments. Don’t put all your eggs in one basket. Spread your investments across different asset classes, such as stocks, bonds, and real estate.

4. Educate Yourself About Finance

To build generational wealth, you need to have a good understanding of personal finance. There are many resources available to help you learn about investing, budgeting, and other financial topics. You can read books, take online courses, or consult with a financial advisor.

- Learn about different investment options. Understand the risks and rewards associated with stocks, bonds, real estate, and other investments.

- Study basic financial concepts. Familiarize yourself with compound interest, risk management, and asset allocation.

- Stay informed about current economic and market trends. Read financial news and publications to stay up-to-date on market developments.

5. Consider Real Estate as an Investment

Real estate can be a valuable asset for building generational wealth. It can provide rental income, appreciate in value over time, and offer tax advantages. However, real estate investing also carries risks, so it’s important to do your research before investing.

- Research local real estate markets. Identify areas with strong rental demand and potential for appreciation.

- Consider different types of real estate investments. From single-family homes to multi-family properties, there are various options to suit different goals and budgets.

- Seek professional advice. Consult with a real estate agent, mortgage lender, or property manager for guidance.

Frequently Asked Questions

What is a financial legacy?

A financial legacy is the wealth and assets that you pass on to your family and loved ones after you pass away. It can include things like cash, investments, property, and other valuable assets. Building a financial legacy is not just about accumulating wealth; it’s about ensuring that your loved ones are financially secure after you’re gone.

Why should I build a financial legacy?

There are many reasons to build a financial legacy. For one, it can provide your family with financial security and stability after you’re gone. It can help them cover expenses, pay off debts, or pursue their dreams. Building a financial legacy can also be a way to leave a lasting impact on your family and community. It’s a way to show your love and support for them and to ensure that their future is bright.

How can I start building a financial legacy?

The first step to building a financial legacy is to set clear goals. What do you want to achieve with your financial legacy? How much do you want to leave behind? Once you have clear goals, you can start to develop a plan. This plan should include strategies for saving, investing, and managing your assets. It’s also important to seek professional advice from a financial advisor to help you create a plan that meets your specific needs.

What are some common mistakes people make when building a financial legacy?

One common mistake is not starting early enough. The earlier you begin saving and investing, the more time your money has to grow. Another mistake is not diversifying your investments. Putting all your eggs in one basket can be risky. Instead, diversify your investments across different asset classes, such as stocks, bonds, and real estate. Finally, many people fail to review and update their financial plan regularly. Your financial goals and circumstances may change over time, so it’s important to review your plan and make adjustments as needed.