Living paycheck to paycheck can be a stressful experience, leaving you feeling trapped and constantly worried about making ends meet. However, it’s important to remember that even when you’re struggling financially, there are steps you can take to avoid accumulating debt. This article will explore practical strategies that can help you manage your finances effectively, build a solid financial foundation, and break free from the cycle of debt.

Here’s the H2 subtitle and a detailed breakdown with H3 subtitles and relevant information:

Living Paycheck to Paycheck? Tips for Avoiding Debt

1. Track Your Spending and Income

Understanding your financial situation is key. Keeping a budget helps you see where your money is going, allowing you to identify areas where you can cut back.

| Category | Monthly Budget | Actual Spending |

|---|---|---|

| Housing | $1,000 | $950 |

| Food | $300 | $400 |

| Transportation | $200 | $180 |

| Utilities | $150 | $160 |

| Entertainment | $100 | $200 |

Pro Tip: Use a budgeting app or spreadsheet to track your spending automatically.

2. Prioritize Essential Expenses

Focus on your needs before your wants. Make sure you’re covering rent, utilities, groceries, and transportation before indulging in non-essentials.

| Essential | Non-Essential |

|---|---|

| Rent/Mortgage | Dining Out |

| Utilities (electricity, water, gas) | Cable TV |

| Groceries | New Clothes |

| Transportation (car payment, gas, public transit) | Subscriptions (streaming services) |

3. Negotiate Bills and Find Savings

Don’t be afraid to negotiate lower rates with your utility companies, phone providers, or insurance companies. Explore discount programs or loyalty programs to save money.

| Company | Negotiation Tips | Savings Potential |

|---|---|---|

| Phone Provider | Call and ask for a loyalty discount or threaten to switch | $20-$50 per month |

| Internet Provider | Bundle services (phone, internet, cable) | $10-$20 per month |

| Insurance Company | Shop around for quotes and leverage multiple policies | $50-$100 per year |

4. Build an Emergency Fund

An emergency fund is crucial for avoiding debt. It provides a safety net to cover unexpected expenses like car repairs, medical bills, or job loss.

| Emergency Fund Goal | Savings Strategy |

|---|---|

| $1,000 | Set aside $50-$100 per week |

| $3,000 | Increase savings to $100-$200 per week |

| $5,000+ | Consider automatic transfers from your checking account to your savings account |

5. Explore Side Hustles and Income Opportunities

Bringing in extra income can help you pay down debt faster or build your emergency fund. Look for side hustles that fit your skills and interests.

| Side Hustle | Earnings Potential | Time Commitment |

|---|---|---|

| Freelancing | $15-$50 per hour | Flexible, part-time or full-time |

| Online Tutoring | $20-$40 per hour | Flexible hours, set your own rates |

| Driving for a Ride-Sharing Service | $15-$25 per hour | Flexible hours, work when you want |

How do I get out of debt when I live paycheck to paycheck?

Create a Budget and Track Your Spending

The first step to getting out of debt is to understand where your money is going. Create a detailed budget that tracks all of your income and expenses. This will help you identify areas where you can cut back. Use a budgeting app or spreadsheet to make tracking easier. You may also want to consider using the 50/30/20 rule, where 50% of your income goes towards needs, 30% goes towards wants, and 20% goes towards savings and debt repayment.

- Track your spending for a month or two to get a clear picture of where your money is going.

- Create a budget that allocates your income to different categories like housing, transportation, food, and debt repayment.

- Stick to your budget and avoid impulse purchases.

- Review your budget regularly and make adjustments as needed.

Reduce Your Expenses

Once you have a budget, look for ways to reduce your expenses. This might involve cutting back on non-essential items like entertainment, dining out, or subscriptions. Consider negotiating lower rates for your bills or switching to a cheaper provider. Small changes can add up over time.

- Identify areas where you can cut back on spending, such as entertainment, dining out, subscriptions, or unnecessary purchases.

- Negotiate lower rates for your bills like utilities, phone, or internet.

- Shop around for cheaper options for things like insurance, groceries, and gas.

- Look for ways to save money on everyday expenses, such as cooking at home more often or using public transportation.

Increase Your Income

While reducing expenses is important, increasing your income can also help you pay off debt faster. Consider getting a second job, asking for a raise, or starting a side hustle. You may also be able to sell unused items or rent out a spare room to generate extra cash.

- Find a second job or take on a freelance gig to increase your income.

- Negotiate a raise at your current job if you feel your contributions are not being reflected in your salary.

- Start a side hustle by leveraging your skills or interests.

- Sell unused items online or at consignment shops to generate extra cash.

Consolidate or Refinancing Your Debt

If you have multiple debts with high-interest rates, you may want to consider consolidating or refinancing them. This can help you reduce your monthly payments and pay off your debt faster. However, make sure to compare different offers and understand the terms and conditions before making a decision. If you are considering consolidating your debt, look for a loan with a lower interest rate than your current debts. This can save you money on interest charges and help you pay off your debt faster.

- Compare different loan options from banks, credit unions, and online lenders.

- Consider a balance transfer credit card with a 0% introductory APR to save on interest charges during the promotional period.

- Be careful with debt consolidation loans as they may extend the repayment term, leading to higher interest charges over time.

Seek Professional Help

If you are struggling to get out of debt on your own, consider seeking professional help from a credit counselor or financial advisor. They can provide personalized advice and support to help you create a debt management plan and achieve your financial goals. A credit counselor can help you develop a budget, negotiate with creditors, and explore options like debt consolidation or debt management plans.

- Consult with a credit counselor for guidance on managing your debt and developing a debt management plan.

- Consider a debt management plan offered by a non-profit credit counseling agency, which may involve negotiating lower interest rates and monthly payments with creditors.

- Seek advice from a financial advisor to gain a deeper understanding of your financial situation and create a personalized plan to achieve your financial goals.

How to survive living paycheck to paycheck?

Create a Realistic Budget

Living paycheck to paycheck can be a stressful experience. It’s important to take control of your finances and create a realistic budget that tracks your income and expenses.

- Track Your Spending: For a few weeks, track every dollar you spend, categorizing each expenditure (e.g., housing, food, transportation, entertainment).

- Identify Areas to Cut Back: After tracking, analyze your spending patterns to identify unnecessary expenses you can reduce or eliminate. Consider using apps like Mint or Personal Capital for automatic tracking.

- Prioritize Needs vs. Wants: Distinguish between essential needs (housing, utilities, groceries) and discretionary wants (dining out, entertainment). Make conscious choices about where to allocate your money.

- Set Financial Goals: Having clear financial goals (e.g., saving for an emergency fund, paying off debt) can provide motivation to stick to your budget.

Build an Emergency Fund

An emergency fund is crucial for surviving unexpected financial challenges.

- Start Small: Even saving a small amount each paycheck can make a difference. Set aside a few dollars every week or month, and gradually increase the amount as your finances improve.

- Automate Savings: Set up automatic transfers from your checking account to a savings account. This helps ensure you regularly contribute to your emergency fund without having to manually make deposits.

- Consider a High-Yield Savings Account: Maximize your savings by choosing a high-yield savings account (HYSA) that offers a higher interest rate than traditional savings accounts.

Negotiate for a Raise or Seek Additional Income

If you’re struggling to make ends meet, consider exploring ways to increase your income.

- Negotiate a Raise: If you’re performing well in your current role, consider discussing a raise with your employer. Research salary ranges for similar positions in your area and gather evidence of your contributions to the company.

- Look for a Side Hustle: Explore opportunities for part-time or freelance work that can supplement your income. Consider gig platforms like Uber, Lyft, or TaskRabbit or freelance platforms like Upwork or Fiverr.

- Sell Unwanted Items: Declutter your home and sell unwanted items online through platforms like eBay, Craigslist, or Facebook Marketplace to generate extra cash.

Reassess Your Debt

High debt can significantly impact your ability to manage your finances.

- Create a Debt Management Plan: Develop a plan to tackle your debt strategically. Consider debt consolidation, debt snowball (paying off smallest debts first), or debt avalanche (paying off highest interest debts first) methods.

- Negotiate Lower Interest Rates: Contact your creditors and try to negotiate lower interest rates on your loans. This can help reduce your monthly payments and free up more money in your budget.

- Consider Debt Consolidation: Explore debt consolidation options, which can help simplify your debt management and potentially lower your overall interest rate.

Seek Professional Guidance

If you’re overwhelmed by your finances, don’t hesitate to seek professional guidance.

- Financial Counseling: A financial counselor can provide personalized advice and support to develop a budget, manage debt, and achieve your financial goals. Look for certified counselors through organizations like the National Foundation for Credit Counseling (NFCC).

- Credit Counseling: Credit counselors can help you understand your credit score, dispute inaccurate information, and develop strategies for improving your creditworthiness.

How bad is living paycheck to paycheck?

:max_bytes(150000):strip_icc()/paycheck-to-paycheck.asp-final-e42b0a5e80094168ae2de4133dc59e09.png)

Living paycheck to paycheck can be incredibly stressful.

Constantly worrying about money can take a toll on your mental and physical health. You might experience anxiety, depression, and even physical symptoms like headaches and insomnia. This constant stress can also lead to unhealthy coping mechanisms, such as overspending or using credit to make ends meet.

It limits your financial flexibility.

When you’re living paycheck to paycheck, you have very little room for unexpected expenses. A sudden car repair, medical bill, or job loss can quickly throw your finances into chaos. This lack of financial flexibility can make it difficult to reach your financial goals, such as saving for retirement or buying a home.

It can impact your relationships.

Financial stress can put a strain on your relationships. You might argue with your partner about money, or feel like you’re constantly asking for help from family and friends. This can lead to resentment and a breakdown in communication.

It can make it difficult to build a good credit score.

If you’re constantly using credit cards to make ends meet, you’re likely racking up debt and interest charges. This can damage your credit score, making it harder to get loans in the future, such as a mortgage or auto loan.

It can hinder your career growth.

If you’re constantly worried about money, it can be difficult to focus on your work. You might be less productive and less likely to take on new challenges. This can limit your career growth and earning potential.

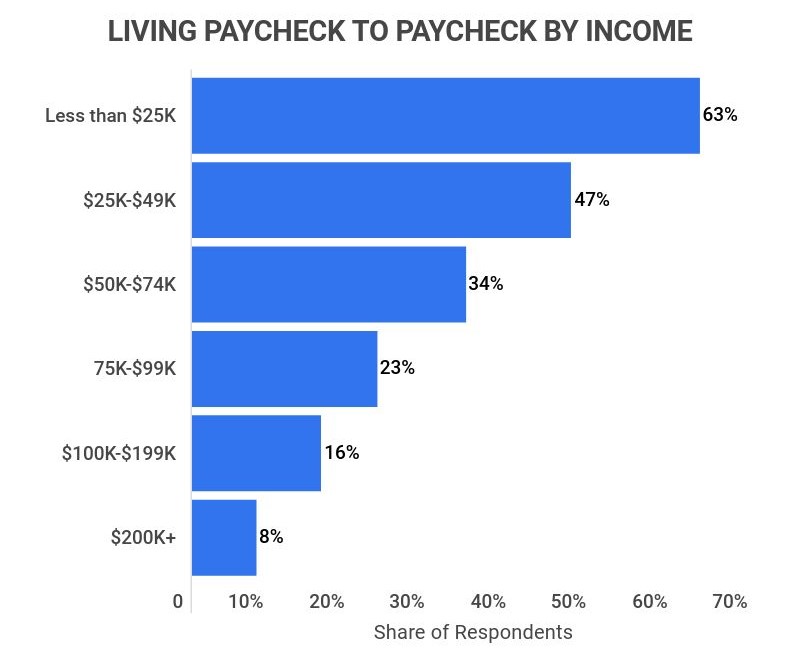

What percent of people who make $100,000 live paycheck to paycheck?

What is considered living paycheck to paycheck?

Living paycheck to paycheck means that an individual is spending all of their income each month, and they have little to no savings. This means that they are living from one paycheck to the next, and if they lose their job or have an unexpected expense, they may struggle to make ends meet.

Factors Affecting Living Paycheck to Paycheck

There are a number of factors that can contribute to someone living paycheck to paycheck, including:

- High cost of living: The cost of housing, transportation, food, and healthcare has been rising in recent years, making it more difficult for people to make ends meet.

- Stagnant wages: Wages have not kept pace with inflation, meaning that people are earning less than they were in the past.

- Debt: High levels of debt, such as credit card debt, student loan debt, or medical debt, can make it difficult to save money and can contribute to living paycheck to paycheck.

- Lack of financial literacy: Many people do not have a good understanding of personal finance, which can make it difficult to budget and manage money effectively.

Living paycheck to paycheck at $100,000 income

It is possible to live paycheck to paycheck even with an income of $100,000. This can happen if an individual has a high cost of living, significant debt, or makes poor financial decisions. Some individuals at this income level also may have a large family with many needs, which makes it difficult to save money.

Survey on Living Paycheck to Paycheck at $100,000 Income

According to a recent survey, 25% of people making $100,000 or more live paycheck to paycheck. This means that they are spending all of their income each month, and they have little to no savings. This suggests that even at a high income level, many individuals are struggling to manage their finances effectively and are not able to save for the future.

Tips to Avoid Living Paycheck to Paycheck

There are a number of things that people can do to avoid living paycheck to paycheck, including:

- Create a budget: A budget helps to track income and expenses and identify areas where you can cut back.

- Save money: It is important to save at least 3-6 months of living expenses in an emergency fund.

- Pay off debt: High levels of debt can make it difficult to save money and can contribute to living paycheck to paycheck.

- Increase income: Explore ways to increase income, such as finding a side hustle or negotiating a raise.

- Reduce expenses: Look for ways to reduce expenses, such as cooking at home more often, using public transportation, or negotiating lower bills.

Frequently Asked Questions

How can I avoid debt when I’m living paycheck to paycheck?

It’s challenging to avoid debt when you’re living paycheck to paycheck, but it’s not impossible. The key is to create a budget that works for you and to stick to it. This means tracking your income and expenses carefully and making sure that you’re not spending more than you earn. You can also look for ways to reduce your expenses, such as negotiating lower interest rates on your debts or cutting back on unnecessary spending. You can even find side hustles to increase your income. It’s also important to have an emergency fund to help you cover unexpected expenses. Having a cushion can help you avoid going into debt when you face an unexpected expense.

What are some ways I can reduce my expenses?

There are many ways to reduce your expenses and live on a tighter budget. One way is to track your spending and see where your money is going. You might be surprised by how much you spend on things you don’t need. Another way to save money is to shop around for better deals on groceries, utilities, and insurance. You can also cook at home more often instead of eating out. Finally, you can cut back on entertainment expenses by finding free or inexpensive activities to do.

I’m already in debt. How can I get out of debt?

Getting out of debt can seem daunting, but it’s possible. The first step is to create a budget and track your income and expenses. This will help you understand where your money is going and identify areas where you can cut back. Once you have a budget in place, you can start developing a debt repayment plan. This plan should prioritize your highest-interest debts and focus on paying them off as quickly as possible. You can also look into debt consolidation or debt management programs. These programs can help you manage your debt and make it easier to pay it off.

What if I have an unexpected expense?

Unexpected expenses can throw off your budget and potentially lead to debt. To avoid this, it’s important to have an emergency fund. This fund should cover at least three to six months of your living expenses. You can build an emergency fund by setting aside a small amount of money each month. It’s also important to have a plan in place for handling unexpected expenses. This plan should include steps for reducing your spending, finding additional income, or taking out a loan. Having a plan in place will help you stay on track and avoid taking on unnecessary debt.