Life insurance is a crucial financial tool for protecting your loved ones financially in the event of your death. However, the cost of premiums can be a significant expense, especially if you have other financial obligations. This article will explore practical strategies for saving money on life insurance premiums and ensure you can afford the coverage you need without breaking the bank. We will discuss factors that influence premium costs, strategies for reducing your premiums, and alternative options to consider.

Saving for Life Insurance Premiums: Strategies for Financial Security

1. Understand Your Needs and Budget

Life insurance premiums can vary greatly depending on factors such as your age, health, coverage amount, and policy type.

Before you start saving, it’s crucial to determine your life insurance needs and establish a budget that comfortably accommodates the premiums. Consider your dependents, financial obligations, and desired coverage.

| Factor | Description |

|---|---|

| Age | Younger individuals typically have lower premiums than older individuals. |

| Health | Good health generally leads to lower premiums. |

| Coverage Amount | Higher coverage amounts result in higher premiums. |

| Policy Type | Different policy types, such as term life or whole life, have varying premium structures. |

2. Set Up a Dedicated Savings Account

Once you know your premium amount, establish a separate savings account specifically for life insurance premiums. This account should be easily accessible but not easily spent.

| Account Type | Benefits |

|---|---|

| High-Yield Savings Account | Offers competitive interest rates, maximizing your savings. |

| Money Market Account | Provides flexibility with withdrawals and potentially higher interest rates than traditional savings accounts. |

3. Automate Your Savings

Automate your savings by setting up recurring transfers from your checking account to your life insurance savings account. This ensures consistent contributions without requiring active effort on your part.

| Automatic Savings Methods | Description |

|---|---|

| Direct Deposit | A portion of your paycheck is directly deposited into your savings account. |

| Recurring Transfers | Regular transfers are scheduled from your checking account to your savings account. |

4. Explore Budgeting Strategies

Consider implementing budgeting strategies to allocate funds efficiently and prioritize saving for life insurance premiums.

| Budgeting Strategy | Description |

|---|---|

| 50/30/20 Rule | Allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. |

| Zero-Based Budgeting | Account for every dollar of your income, ensuring that all expenses are budgeted and any remaining funds are saved. |

5. Consider Financial Products

Explore financial products that can help you save for your life insurance premiums.

| Financial Product | Description |

|---|---|

| High-Yield Savings Account | Offers competitive interest rates, maximizing your savings. |

| Certificates of Deposit (CDs) | Fixed-term investments with guaranteed interest rates. |

How to save money on life insurance premiums?

Life insurance is an important investment, but it can also be expensive. Fortunately, there are a number of things you can do to save money on your premiums. Here are some tips:

Shop around for the best rates

- Life insurance rates can vary widely from company to company. It is important to shop around and compare quotes from several different insurers before you make a decision.

- You can use an online comparison tool or contact an insurance broker to get quotes from multiple companies.

- Make sure to compare apples to apples when you’re comparing rates. Look at the same type of coverage, death benefit, and policy terms.

Increase your deductible

- If you have a term life insurance policy, you can often save money by increasing your deductible. This means that you will have to pay more out of pocket if you need to file a claim, but you will also pay lower premiums.

- You should make sure that you can afford the higher deductible before you increase it.

- A higher deductible can make your premiums more affordable, but it is important to make sure that you can still afford to pay for the deductible if you need to file a claim.

Consider a shorter policy term

- Term life insurance policies are typically less expensive than permanent life insurance policies. This is because term life insurance policies only cover you for a specific period of time, such as 10, 20, or 30 years.

- If you only need life insurance for a limited time, such as while you are raising children or paying off a mortgage, a term life insurance policy can be a good option.

- Term life insurance policies provide affordable coverage for a limited period of time.

Improve your health

- Life insurance companies typically charge lower premiums to people who are in good health.

- If you have any health issues, you can work to improve your health to qualify for a lower premium. This can include things like losing weight, quitting smoking, and controlling your blood pressure.

- Maintaining good health is beneficial for your overall well-being and can also help you qualify for lower premiums.

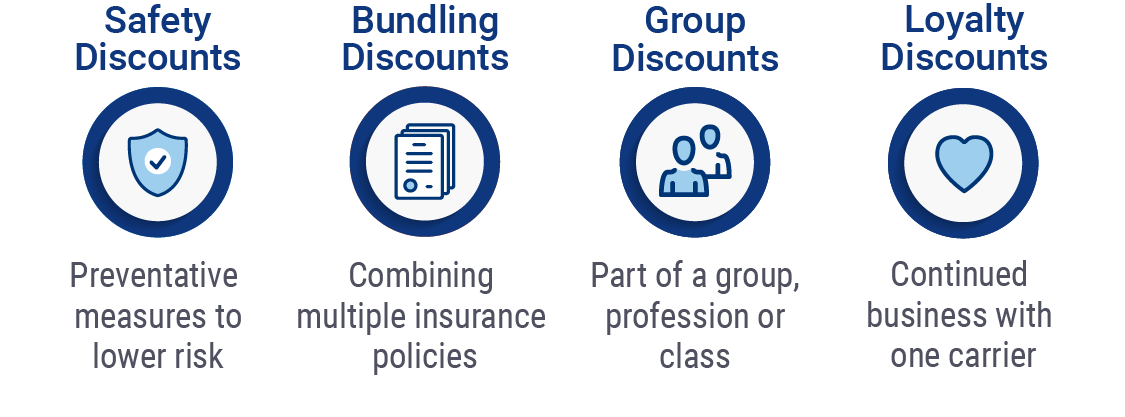

Bundle your insurance policies

- Many insurance companies offer discounts if you bundle your insurance policies with them. This means that you can save money on your life insurance premiums if you also purchase car insurance, home insurance, or other types of insurance from the same company.

- Bundling your insurance policies can be a simple way to save money. Contact your insurance company to see if they offer any discounts for bundling.

Can you reduce your life insurance premiums?

Yes, there are several ways you can potentially reduce your life insurance premiums. The specific options available to you will depend on your individual circumstances and the type of policy you have. However, some general strategies you can consider include:

Shop around for a better rate.

Just like with any other financial product, it’s a good idea to compare quotes from multiple life insurance companies. You may be able to find a lower rate with a different provider, especially if you have a good credit score and a healthy lifestyle.

Increase your deductible.

Similar to how you can increase your deductible on your auto or home insurance to lower your monthly premiums, you can also increase your deductible on your life insurance policy. This means that you’ll pay more out-of-pocket if you need to file a claim, but you’ll also pay less in premiums over time.

Consider a term life insurance policy.

Term life insurance policies are typically cheaper than permanent life insurance policies. This is because they only provide coverage for a specific period of time, usually 10, 20, or 30 years. If you’re only looking for coverage for a limited period of time, a term life insurance policy may be a more affordable option.

Make sure your policy is tailored to your needs.

Are you paying for more coverage than you need? If you’ve recently paid off your mortgage or your children have grown up, you may be able to reduce your coverage amount and, in turn, your premiums.

Consider paying your premiums annually.

Paying your premiums annually rather than monthly can often result in a discount. This is because life insurance companies typically offer discounts for those who pay in full.

At what age should you stop paying life insurance?

There is no set age to stop paying for life insurance.

There is no one-size-fits-all answer to the question of when to stop paying for life insurance. It is a personal decision that should be based on your individual circumstances, including your age, health, financial situation, and the needs of your dependents.

Factors to consider when deciding whether to stop paying for life insurance.

- Your age and health: As you age, your life expectancy decreases. If you are in good health, you may be able to get a lower premium on a new policy or simply let your existing policy lapse. However, if you have pre-existing health conditions, you may need to continue paying for life insurance to ensure your loved ones are financially protected.

- Your financial situation: If you have a substantial amount of savings and investments, you may be able to self-insure and stop paying for life insurance. However, if your financial situation is precarious, you may need to continue paying for life insurance to protect your family from financial hardship in the event of your death.

- Your dependents’ needs: If you have children or a spouse who rely on your income, you may need to continue paying for life insurance until your children are financially independent or your spouse is no longer dependent on you.

- The cost of your life insurance policy: As you age, your life insurance premiums may increase. If the cost of your policy becomes prohibitive, you may want to consider stopping your payments or switching to a less expensive policy.

- The value of your life insurance policy: If your life insurance policy has a high death benefit, it may be worthwhile to continue paying for it, even if you are older. However, if the death benefit is low, you may want to consider stopping your payments and using the money for other purposes.

The pros and cons of stopping life insurance payments.

- Pros: Stopping life insurance payments can free up cash flow that you can use for other purposes. You may also be able to save money on your premiums.

- Cons: If you stop paying for life insurance, your loved ones will not receive a death benefit if you pass away. This could leave them financially vulnerable.

Alternatives to stopping life insurance payments.

- Reduce your death benefit: If you want to keep your life insurance policy but reduce your premiums, you can reduce your death benefit. This will lower your premiums but also decrease the amount of money your loved ones will receive if you pass away.

- Convert your term life insurance policy to a permanent policy: If you have a term life insurance policy, you may be able to convert it to a permanent policy. This will allow you to pay premiums for the rest of your life, but you will also have a death benefit that is guaranteed to pay out.

- Take out a smaller life insurance policy: If you need life insurance but can’t afford a large policy, you can take out a smaller policy. This will provide your loved ones with some financial protection, but the death benefit will be smaller.

Consult a financial advisor.

It is always a good idea to consult with a financial advisor before making any major decisions about your life insurance. A financial advisor can help you assess your individual needs and make the best decision for your situation.

How to get a discount on life insurance?

How to Get a Discount on Life Insurance?

Here’s a detailed breakdown of how to get a discount on life insurance:

Shop Around and Compare Quotes

The first and most important step is to shop around and compare quotes from multiple life insurance companies. This is essential because insurance companies use different pricing models and offer different discounts.

Use online comparison websites: These websites allow you to enter your information once and get quotes from multiple companies.

Contact insurance agents directly: Talking to an agent can give you personalized advice and help you understand the different options available.

Check for discounts offered by your current insurer: Some insurance companies offer discounts to existing customers who purchase additional policies.

Improve Your Health Habits

Many life insurance companies offer discounts to policyholders who maintain healthy habits. Here are a few things you can do:

Quit smoking: This is one of the most significant factors affecting life insurance premiums. Quitting smoking can significantly lower your rates.

Maintain a healthy weight: Being overweight or obese can increase your risk of certain health conditions, which can lead to higher premiums.

Exercise regularly: Staying active can help you maintain a healthy weight and reduce your risk of chronic diseases.

Get regular health screenings: These screenings can help you identify and address health issues early, which can lower your risk of developing more serious problems.

Bundle Your Policies

Some insurance companies offer discounts to customers who bundle their policies. This means purchasing multiple types of insurance, such as life insurance, home insurance, and car insurance, from the same company.

Ask your insurer about bundling discounts: If you’re already a customer, inquire about any discounts you might be eligible for by adding another type of insurance policy.

Compare quotes from different insurers: See if bundling with one insurer is more advantageous than buying separate policies from different companies.

Choose a Longer Policy Term

Life insurance policies are typically offered for a specific term, such as 10, 20, or 30 years. Generally, choosing a longer policy term can lead to lower premiums per year.

Consider your long-term needs: A longer term policy may provide more coverage for your family and loved ones.

Evaluate your financial situation: Ensure that you can afford the premiums for a longer policy term.

Increase Your Deductible

Life insurance policies typically have a deductible, which is the amount you pay out of pocket before the insurance company begins to cover your costs. Increasing your deductible can often result in lower premiums.

Assess your risk tolerance: A higher deductible means you’ll have to pay more in the event of a claim.

Calculate the potential savings: Make sure the savings from a higher deductible outweigh the risk of a larger out-of-pocket expense.

Frequently Asked Questions

How much should I save for life insurance premiums?

The amount you should save for life insurance premiums depends on several factors, including the type of policy you want, the coverage amount you need, and your age and health. It’s best to start by determining your financial needs and then considering your budget and the cost of different life insurance policies. A financial advisor can help you determine the right amount of coverage for you and your family, and then you can work out a savings plan to pay for the premiums.

Where is the best place to save for life insurance premiums?

There are several places where you can save for life insurance premiums, including high-yield savings accounts, money market accounts, or certificates of deposit (CDs). It’s important to choose an account that offers a competitive interest rate and allows you to access your funds easily. You should also consider opening a separate savings account specifically for life insurance premiums so that you don’t spend the money on other things.

How do I make sure I’m saving enough for life insurance premiums?

There are a few ways to make sure you’re saving enough for life insurance premiums. First, create a realistic budget and allocate a specific amount of money to your life insurance savings each month. You can also consider setting up automatic transfers from your checking account to your savings account. Finally, it’s important to review your savings plan regularly to ensure you’re on track to meet your goals.

What happens if I can’t afford to pay my life insurance premiums?

If you’re unable to pay your life insurance premiums, it’s important to contact your insurance company as soon as possible. They may offer you options such as a payment plan or a loan. In some cases, your policy may lapse if you don’t make your premium payments, which means you will lose your coverage. However, depending on the policy, it may be possible to reinstate your policy if you pay back your missed premiums.