Here’s an introduction for an article on «The Role of Savings in Achieving a Debt-Free Lifestyle»:

**Option 1 (Short and punchy):**

Living debt-free is a financial goal many aspire to. While diligently paying down debt is crucial, often overlooked is the power of saving. This article explores how saving, even small amounts, can significantly accelerate your journey to a debt-free life and ultimately create a more secure financial future.

**Option 2 (More detailed):**

The allure of a debt-free life is undeniable: increased financial freedom, reduced stress, and the ability to pursue your passions. While many focus on debt reduction strategies, the role of saving often takes a backseat. However, a strong savings strategy can be the missing piece in your quest for financial independence. This article examines the interconnected relationship between saving and debt reduction, demonstrating how even modest savings can fuel your journey towards a debt-free lifestyle. We’ll explore practical strategies and mindset shifts that can help you build a substantial savings cushion, ultimately empowering you to achieve your financial goals.

The Role of Savings in Achieving a Debt-Free Lifestyle

The Role of Savings in Achieving a Debt-Free Lifestyle

Understanding the Connection Between Savings and Debt Reduction

Saving money plays a crucial role in achieving a debt-free lifestyle. While it may seem counterintuitive to save money while also trying to pay off debt, the two are deeply interconnected. Saving money allows you to build a financial safety net and provides you with the resources to attack your debt more aggressively.

| Saving | Debt Reduction |

|---|---|

| Provides financial security and peace of mind. | Reduces stress and anxiety associated with debt. |

| Offers a buffer for unexpected expenses, preventing further debt accumulation. | Allows you to allocate more funds towards debt repayment. |

| Empowers you to make smart financial decisions, including debt consolidation or early payoff. | Leads to improved credit score and financial stability. |

Building an Emergency Fund

An emergency fund is a crucial component of a debt-free lifestyle. It acts as a financial safety net that protects you from unexpected expenses, preventing you from falling back into debt. Having an emergency fund allows you to cover unforeseen costs like medical bills, car repairs, or job loss without resorting to credit cards or high-interest loans.

| Emergency Fund | Debt-Free Lifestyle |

|---|---|

| Provides a buffer for unexpected expenses. | Prevents the need to rely on high-interest debt for emergencies. |

| Reduces financial stress and anxiety. | Promotes financial stability and independence. |

| Allows you to focus on paying off existing debt without worrying about unexpected costs. | Creates a stronger foundation for long-term financial success. |

Prioritizing Debt Repayment

Once you have an emergency fund in place, you can start prioritizing debt repayment. Saving money can accelerate this process, allowing you to make larger payments and pay off debt faster. By saving extra funds, you can make lump-sum payments towards your highest-interest debt, reducing the overall amount of interest you pay and speeding up the debt-free journey.

| Saving | Debt Repayment |

|---|---|

| Provides extra funds for lump-sum payments. | Reduces interest charges and accelerates debt payoff. |

| Allows you to focus on high-interest debt first, minimizing interest accumulation. | Creates a sense of progress and motivates further savings. |

| Increases financial flexibility and reduces the burden of debt. | Empowers you to make informed financial decisions for a debt-free future. |

Developing a Savings Plan

A well-defined savings plan is essential for achieving a debt-free lifestyle. This plan should outline your savings goals, target amounts, and timeline. It helps you stay motivated and track your progress, ensuring that you are consistently saving towards your financial goals.

| Savings Plan | Debt-Free Lifestyle |

|---|---|

| Provides clear goals and targets for savings. | Keeps you focused on the path to financial freedom. |

| Tracks your progress and motivates you to stay on track. | Promotes financial discipline and responsibility. |

| Enables you to make informed financial decisions based on your savings goals. | Leads to a more structured and sustainable approach to debt management. |

Creating a Budget

A well-crafted budget is fundamental for both saving and debt reduction. By tracking your income and expenses, you gain insights into your spending habits and identify areas where you can reduce unnecessary spending. This allows you to allocate more funds towards savings and debt repayment, ultimately accelerating your journey towards financial freedom.

| Budget | Debt-Free Lifestyle |

|---|---|

| Tracks income and expenses, identifying spending patterns. | Provides a clear understanding of your financial situation. |

| Identifies areas for cost-cutting and savings optimization. | Allows you to allocate more funds towards debt repayment and savings. |

| Promotes financial discipline and accountability. | Encourages mindful spending and responsible financial management. |

What is the role of savings in the financial system?

Savings as a Source of Funds for Investment

Savings play a crucial role in the financial system by acting as a source of funds for investment. When individuals and businesses save, they are essentially putting money aside for future use. This saved money is then channeled into the financial system through various channels, such as banks, credit unions, or investment funds. These institutions then lend or invest these funds to borrowers, such as businesses, individuals, or governments, who need capital for expansion, consumption, or public projects. This flow of funds from savers to borrowers facilitates economic growth and development.

Savings and Economic Growth

The level of savings in an economy is a key driver of economic growth. When individuals and businesses save a higher proportion of their income, it frees up more resources for investment, which in turn leads to increased productivity, job creation, and higher living standards. A strong savings rate is essential for long-term economic prosperity.

Role of Savings in Financial Stability

Savings contribute to financial stability by providing a buffer against economic shocks. During periods of economic downturn, individuals and businesses with accumulated savings can draw upon these reserves to weather the storm. This reduces the need for excessive borrowing, which can exacerbate financial instability. A healthy savings rate helps to mitigate financial risks and promote economic resilience.

Impact of Savings on Interest Rates

The level of savings in an economy can also influence interest rates. When savings are abundant, the supply of loanable funds increases, which tends to put downward pressure on interest rates. Conversely, when savings are scarce, the demand for loanable funds outweighs the supply, leading to higher interest rates. Interest rates, in turn, affect investment decisions, consumption patterns, and the overall level of economic activity.

Savings and Capital Formation

Savings are essential for capital formation, which is the process of creating new physical assets, such as machinery, buildings, and infrastructure. By providing the funds for investment, savings enable businesses to expand their operations, purchase new equipment, or build new facilities. This investment in capital goods leads to increased productivity, higher output, and economic growth.

Is it better to be debt free or have savings?

The Importance of Both Debt Freedom and Savings

The question of whether it’s better to be debt-free or have savings is a common one, and the answer is: it depends. Both are crucial aspects of financial well-being, and the ideal situation is to achieve both. However, the path to reach that point can vary depending on your individual circumstances and financial goals.

Debt Freedom: The Foundation of Financial Security

Being debt-free offers several advantages:

- Reduced financial stress: Debt can be a significant source of anxiety and worry.

- More disposable income: With no debt payments, you have more money available for other expenses, savings, and investments.

- Improved credit score: Paying off debt helps boost your credit score, making it easier to access credit in the future with lower interest rates.

Savings: A Buffer for Uncertainties

Savings provide a safety net for unexpected events.

- Emergency fund: Having savings can cover unexpected expenses like medical bills, car repairs, or job loss.

- Financial goals: Savings allow you to work towards your financial goals, such as buying a house, investing, or retiring early.

- Peace of mind: Knowing you have a financial cushion can reduce stress and provide peace of mind.

Prioritizing Debt Elimination

In some cases, it might be more beneficial to prioritize paying off debt before focusing on saving.

- High-interest debt: If you have high-interest debt, such as credit cards or payday loans, it’s essential to tackle those first. The longer you carry high-interest debt, the more interest you accrue, and the harder it becomes to get ahead financially.

- Debt snowball method: This method involves listing your debts from smallest to largest and paying the minimum on all debts except the smallest one. Once the smallest debt is paid off, you roll that payment amount onto the next smallest debt, and so on. This can provide a sense of accomplishment and motivate you to keep going.

Balancing Debt Reduction and Savings

Ideally, you can strike a balance between paying down debt and building savings.

- Emergency fund first: Start by building a small emergency fund, ideally 3-6 months of living expenses. This will help you avoid going into debt for unexpected expenses.

- Debt snowball/avalanche: Once you have an emergency fund, focus on paying off debt using either the debt snowball or debt avalanche method. The debt avalanche method prioritizes debts with the highest interest rates first.

- Regular saving: While paying off debt, try to save a small amount regularly. Even if it’s just a few dollars per week, it will add up over time.

How can saving money give you freedom?

Saving money gives you the freedom to pursue your passions

Saving money gives you the freedom to pursue your passions by allowing you to take risks and make investments that you wouldn’t be able to otherwise. For example, if you’ve always dreamed of starting your own business, saving money can give you the financial security to take the leap and pursue your dream. Or, if you’ve always wanted to travel the world, saving money can give you the freedom to book those flights and explore new cultures.

Saving money gives you the freedom to be spontaneous

Saving money gives you the freedom to be spontaneous by allowing you to take advantage of opportunities that you wouldn’t be able to otherwise. For example, if you come across a great deal on a vacation or a concert ticket, you can purchase it without having to worry about whether or not you can afford it. Or, if you get an unexpected opportunity to change jobs or move, you can take advantage of it without having to worry about the financial implications.

Saving money gives you the freedom to make choices

Saving money gives you the freedom to make choices by allowing you to live within your means and avoid debt. If you have a good financial cushion, you’re not forced to take on debt to cover unexpected expenses. And you’re not forced to make choices that you don’t want to make just because you’re strapped for cash. For example, you can choose to take a lower-paying job that you love, or you can choose to live in a smaller home in a neighborhood that you prefer. You’re not limited by your finances, so you can make choices that are in your best interest.

Saving money gives you the freedom to be secure

Saving money gives you the freedom to be secure by allowing you to build a safety net that you can rely on in times of need. If you lose your job, get sick, or experience some other unexpected event, you’ll have a financial cushion to fall back on. This can help you avoid falling into debt and give you peace of mind knowing that you can weather any storm.

Saving money gives you the freedom to retire early

Saving money gives you the freedom to retire early by allowing you to build up a nest egg that will provide for you in your later years. The more money you save, the sooner you can retire and enjoy the fruits of your labor. This can be a huge benefit, as it allows you to enjoy your retirement years to the fullest and to spend more time with loved ones.

How saving contributes to financial well being?

Financial Security

Saving money builds a financial safety net. It provides a cushion to fall back on during unexpected events like job loss, medical emergencies, or home repairs. Having savings can alleviate stress and anxiety, knowing you have resources to handle life’s curveballs. A substantial emergency fund can prevent you from relying on high-interest loans or dipping into your retirement funds.

Achieving Goals

Saving is essential for reaching your financial goals, whether it’s buying a house, financing your education, starting a business, or taking a dream vacation. By setting saving goals and consistently contributing, you’re actively working towards your aspirations. The more you save, the faster you can achieve your goals, giving you a sense of accomplishment and motivation to continue.

- Buying a house: Saving for a down payment is a major step in homeownership. Having a larger down payment reduces the amount you need to borrow, resulting in lower monthly mortgage payments and potentially a lower interest rate.

- Financing education: Saving for college or trade school can help cover tuition, fees, and living expenses, reducing the need for student loans and the burden of future debt.

- Starting a business: Saving for startup costs, inventory, marketing, and unexpected expenses can give your business a solid foundation and increase its chances of success.

- Taking a dream vacation: Saving for a special trip allows you to enjoy a memorable experience without stressing about finances. It can be a reward for your hard work and a source of long-lasting memories.

Building Wealth

Saving is the cornerstone of wealth building. It allows you to accumulate assets over time, which can grow through investments like stocks, bonds, and real estate. The more you save, the more you have to invest, potentially earning higher returns and building wealth faster. Compounding interest, where your earnings generate more earnings, is a powerful force for long-term wealth growth.

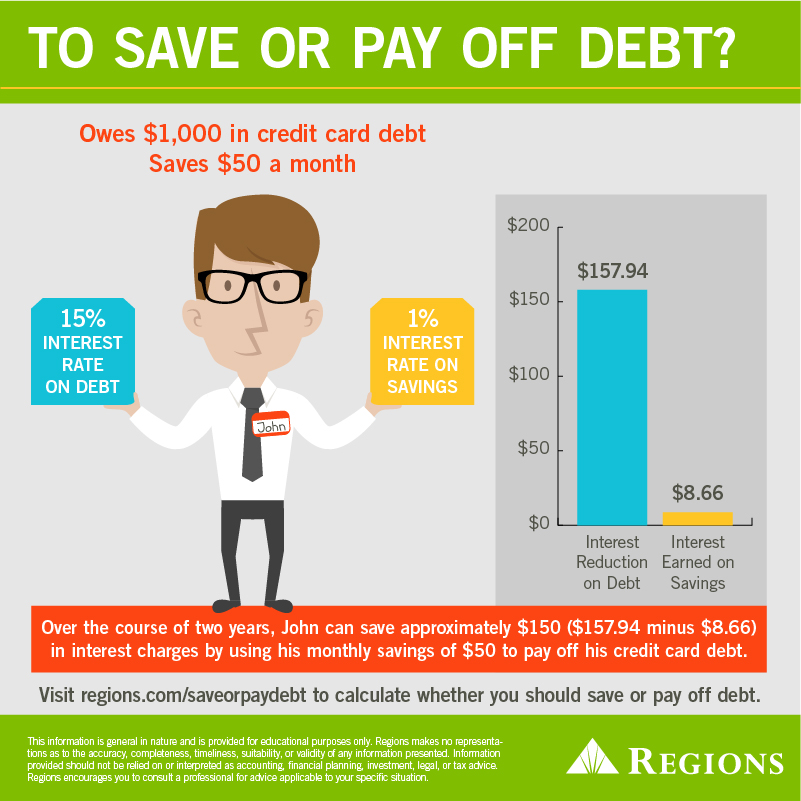

Reducing Debt

Saving can help you pay down debt more efficiently. When you have a savings cushion, you can make extra payments on your loans, reducing the principal balance and the amount of interest you pay over time. A debt-free lifestyle is a significant contributor to financial well-being, freeing up more of your income for other priorities.

Investing in Your Future

Saving is an investment in your future. It secures your financial independence and provides peace of mind for you and your loved ones. A strong savings foundation can give you options and flexibility in your later years, allowing you to retire comfortably, pursue new interests, or help your family.

Frequently Asked Questions

Why are savings important for becoming debt-free?

Saving money is a crucial step toward achieving a debt-free lifestyle. When you save, you’re essentially building a financial safety net. This safety net acts as a buffer against unexpected expenses, preventing you from relying on credit and accumulating more debt. By having readily available savings, you can avoid the high interest rates associated with credit cards and loans. This allows you to prioritize paying off your existing debts faster, leading to a quicker path to financial freedom. Additionally, saving for specific financial goals, like a down payment on a house or starting a business, can give you the financial leverage you need to avoid debt altogether. Therefore, building a strong savings habit is essential for effectively managing debt and achieving a debt-free lifestyle.

How can I prioritize savings while paying off debt?

Prioritizing savings while simultaneously paying off debt can feel daunting, but it’s entirely achievable with a strategic approach. The key is to allocate your income effectively, focusing on both debt reduction and savings. Start by creating a detailed budget that outlines your income, expenses, and debt payments. This will provide a clear picture of your financial situation. Next, consider using the «snowball» or «avalanche» method for debt repayment. The snowball method focuses on paying off the smallest debts first, gaining momentum and creating a sense of accomplishment. Meanwhile, the avalanche method targets the debt with the highest interest rate first, resulting in long-term savings. While focusing on debt repayment, allocate a small amount of your income to a savings account. Even a modest amount can make a difference over time. By prioritizing both debt reduction and savings, you can move towards a debt-free future while also building financial security.

What are some effective saving strategies for becoming debt-free?

Several effective saving strategies can help you achieve a debt-free lifestyle. One crucial step is to identify and eliminate unnecessary expenses. This involves scrutinizing your budget, identifying areas where you can cut back, and negotiating lower rates for services like cable or internet. Consider exploring cost-effective alternatives for entertainment and dining out. Additionally, automating your savings can be incredibly beneficial. Set up automatic transfers from your checking account to your savings account, making saving a consistent habit. Lastly, consider exploring ways to generate additional income. This could involve taking on a side hustle, selling unused items, or leveraging your skills for freelance work. By implementing these strategies, you can increase your savings while simultaneously tackling your debt, accelerating your journey to financial freedom.

What role does financial discipline play in becoming debt-free?

Financial discipline is the cornerstone of achieving a debt-free lifestyle. It involves making conscious choices about how you spend, save, and manage your money. This requires developing self-control and resisting impulsive purchases, even when faced with tempting offers. By practicing financial discipline, you can resist the allure of credit and prioritize paying off existing debts. It also involves budgeting effectively, setting realistic financial goals, and tracking your progress. Cultivating financial discipline can be a lifelong journey, requiring patience, consistency, and a commitment to responsible financial management. This disciplined approach will empower you to make informed financial decisions, avoid debt traps, and ultimately achieve your goal of becoming debt-free.